The Binance Settlement is an Armistice and the Bitcoin ETF is a Trade Deal

The Binance Settlement is an Armistice and the Bitcoin ETF is a Trade Deal

The Government and Crypto are Making Nice

After 5 years of investigation, the DOJ has finally settled with Binance over money-laundering and sanctions violations allegations for $4 billion.

The settlement removes a big cloud from over the crypto space and, in my mind, is representative of a thawing stance toward the industry from regulators and government agencies.

Why now?

With the SEC taking a slew of losses this year both in the courts (lost case against Ripple, appears set to lose case or settle with Coinbase, Grayscale appeal for GBTC ETF conversion was upheld) and in the court of public perception (was cozy with FTX before fraud was exposed), the simple answer is that the political winds have shifted and the chorus of voices asking to move the industry forward in a constructive and non-adversarial way has grown too loud to ignore.

Related to this would be a growing acceptance among TradFi insitutions of the 1) the demand for market access to cryptoassets among their clients and 2) the inevitable adoption of public blockchains to improve upon existing financial market structure. Cheaper and faster inevitably wins in technology.

The most visible of the current initiatives to merge tradfi and crypto is the BlackRock Bitcoin ETF application. The uncertainty surrounding Binance, the largest spot bitcoin volume exchange globally, likely represented a hurdle for the ETF approval, and a settlement now likely echos the pressure to bring a spot bitcoin ETF to market and makes a January approval all but a certainty.

Viewing the timing through a more cynical lens, we are entering an election year and as everyone knows, as the economy/stock market goes, so goes the incumbent party’s chances of reelection. With surveys indicating now >20% of Americans own some crpyto, it’s quite possible that Yellen Claus got on the phone with Goldman Gary and Merrick Garland and instructed them to pump those bags in time for Christmas.

It’s also possible that it was deemed tearing Binance down to the studs would cause too much financial harm to too many individuals — i.e. Binance has become “Too Big Too Fail.”

Whatever the case may be, I believe for the investor in the space that the Binance settlement with the DOJ is best viewed as an armistice, and the Bitcoin ETF viewed as a trade deal.1

The Bitcoin ETF is a Trade Deal

Put aside all bitcoin vs. crypto talk for a day.

No matter your views on that debate, the current reality is that the overlap of investors holding bitcoin and other digital assets is high, and the value of these assets is highly correlated.

So when I say the bitcoin ETF is a trade deal, what I mean is it is going to open up the floodgates for capital to flow from TradFi into crypto, and this is a rising tide that is going to lift all boats.

What do newly rich bitcoin holders do? They speculate on shitcoins.

What do newly rich shitcoin holders do? They speculate on NFTs.

I’m not saying this is right, or wrong, or productive in any way. Just that it is.

Combine the flow of capital into the space enabled by the spot bitcoin ETF with:

The election cycle

The bitcoin halving

Massive fiscal deficits

The ongoing, inevitable, mathematical need to monetize the growing national debt

And it’s hard not to be bullish as we head into 2024.

Sniffing Out The End Game

In Flight to Quality (10/25), I argued that I thought the bitcoin rally at the time was more likely sniffing out an imminent change in central bank liquidity provisions than it was merely front-running spot ETF approval.

At the time, bond yields were soaring and my thesis was that the Fed was going to have intervene in the bond market either through QE (buying treasuries — i.e. monetizing the debt) or Yield Curve Control (YCC), which are two sides of the same coin:

QE: we’ll buy a fixed amount of bonds at any price

YCC: we’ll buy an unlimited amount bonds at a fixed price

I mentioned I was watching boomer bitcoin (gold) as a signal for whether the bitcoin move was idiosyncratic (i.e. potentially due to bitcoin-specific factors such as the ETF approval), or if it was indeed a harbinger for global liquidity conditions.

Since that time, bitcoin has continued it’s rally from $30k to just shy of $44k as I write this, and gold has corroborated by pushing above $2k/oz to new all-time highs.

That said, a lot has shifted since 10/25, most notably the US Treasury’s decision to up their issuance of bills relative to coupons as covered in Yellen Claus Saves Christmas (11/3). In the wake of this announcement, bond yields have fallen, lessening the need to restart QE, but at the same time the Treasury has signalled to the market that the it is willing to deviate from typical policy in order to goose the economy and markets as we head into an election year.

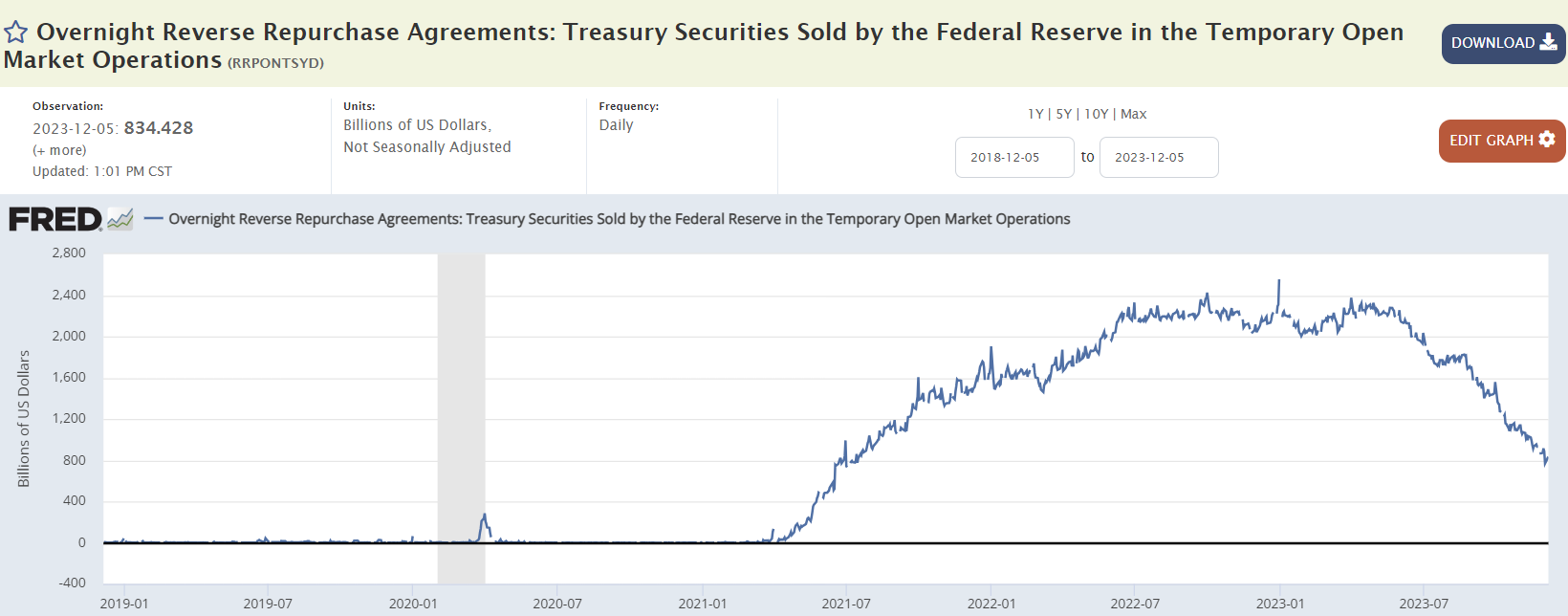

I continue to think that the draining of the RRP will mark the handing of the baton from the Treasury to the Fed, and the cooling inflation backdrop gives the Fed cover to start lowering interest rates and, if need be (and I suspect it will be needed), resuming QE in 2024.

Since 11/3, the RRP has fallen by another $150 billion to currently sit at $834 billion:

At the rate of decline since June, the RRP will be drained in the next ~4 months, or sometime between mid-March and mid-April 2024.

Before we get too bulled up on the current environment, I want to point out that I think bitcoin will likely act as the canary in the coal mine for risk assets throughout 2024, and as such I will be watching the price action closely as the RRP approaches zero.

Again, my best guess is a short, sharp, painful drawdown in risk assets when the RRP runs out, to be met with the return of QE and subsequently rocket emojis everywhere in short order.

The caveat to this thesis is if the Fed resumes QE before the RRP is drained in support of the treasury market we may never see the drawdown I anticipate. I assign this outcome low probability, but we will know ahead of the draining of the RRP one way or the other.

How high can bitcoin rally between now and then? I have no idea.

As always, I could also be completely wrong.

Perhaps the market is more forward looking than I give it credit for, and it will ignore any short-term liquidity shocks with the knowledge any shortage of liquidity can and will only be met with one thing: more liquidity. In this case, the short, sharp drawdown I fear may never materialize.

On the other hand, perhaps inflation perks back up and the Fed prioritizes stamping it out over financial market stability, raising rates further and causing more stress on the banking system until another bank goes under or something else “breaks.” In this case, short and sharp might be longer and sharper than many investors expect or can tolerate.

Of course, it bears mentioning, this is all speculation on what is to come over the next 6-12 months.

If you have the resources and temperament to think and act long-term, you may or may not care about any of this.

To be clear, I maintain my view that over the medium and long-term (5+ years) I think bitcoin will be the best performing asset for the forseeable future.

The Roadmap for TradFi x Crypto

I thoroughly enjoyed this Ethereum Investment Framework from Token Terminal and recommend the whole report to interested investors. It provides many easy-to-grasp analogies between public blockchains and other open standards/protocols upon which products and services are built, including TCP/IP (Transmission Control Protocol/Internet Protocol), VOIP (Voice Over Internet Protocol) and SMTP (Simple Mail Transfer Protocol).

The hallmark of these open protocols is interoperability. This is what allows gmail, yahoo, outlook, and whatever other email client you use to work seamlessly together — they’re all built on-top the same SMTP protocal and thus interoperable.

Contrast this to our current global financial system, which is completely inoperable.

You can’t send money from CashApp to PayPal (like you can send an email from gmail to yahoo), nor from the US to Mexico, nor from your bank account to your merchant’s bank account, without going through a series of intermediaries, who all charge a fee. Companies like Stripe and Plaid exist to provide the connective tissue between private ledgers maintained by banks.

Contrast this with a transaction on a public blockchain that settles peer-to-peer, instantly, and at near-zero cost between everyone is on the same public ledger.

In the report, the authors lay out a compelling roadmap for the future merger of TradFi and DeFi:

As mentioned, we expect early mover traditional finance firms to win together with quality crypto networks and protocols.

An analogy from web2 is how Microsoft and Google leverage the SMTP protocol to deliver email services to end users. SMTP is a permissionless, open-source internet protocol that provides the infrastructure for Microsoft, Google, etc. to build email services “on top” of.

Ultimately, we think that firms such as Blackrock, Fidelity, etc. will be competing to offer new products and services by tapping into public blockchains and DeFi protocols — opening up net new markets. With that said, we expect this to be a slow, phased approach. Below is a rough overview of how we think it could progress in the coming years. Keep in mind that many of these products are already making their way into the market.

Offer trading and custody of large cap crypto assets such as Bitcoin & Ethereum

Offer Bitcoin and Ethereum as options within 401ks and Mutual Funds

Launch Bitcoin ETFs

Launch Ethereum ETFs

Tokenized Treasuries and Money Market Accounts

Tokenized Equities

Offer Separately Managed Accounts covering a basket of crypto infrastructure projects

Launch ETFs covering a basket of L1 projects

Launch ETFs covering a basket of DeFi protocols

Offer trading of a broader range of crypto assets

Offer staking services to customers — allowing them to earn yield on their crypto assets

Provide buy/sell side analysis of crypto networks and protocols utilizing on-chain data & analytics platforms such as Token Terminal

Integrate with DeFi protocols via Ernst & Youngs (and other) privacy enabled L2 Nightfall

Provide the access points for users to do on-chain lending/borrowing, asset management, and provide liquidity to decentralized exchanges (yield generating activities)

Offer access to private, tokenized assets such as Commercial Real Estate and Private Equity (with additional services delivered via DeFi integrations)

Financialization of NFTs and nearly anything with a yield

Provide insurance for self-custody wallets

Ultimately, we expect all assets to be tokenized and all of finance to run on public blockchains. If history is any indication, it could take about 10 years for half of the market to port products, services, and assets over to public blockchains from the “go moment” (clear regulations & market acceptance/consensus). This would be in line with the recent migration timeline for enterprises to the cloud.

What this vision represents is not an adversarial relationship between the legacy financial system and crypto, but a complementary one in which the new, faster, cheaper tech is used to update the old system.

And the first major step between the merging of these economies is the trade deal that is the spot bitcoin ETF.

If we continue to emerge from the bear market we’ve been in, it surely will be tempting to ring the register and take victory laps.

You didn’t survive, study, learn, and earn conviction through the last bear market just to get back above water.

Stay humble, stack sats, zoom out, and remember that it is all still to play for:

None of this is financial advice.

Please do your own research.

Good luck.