Yellen Claus Saves Christmas

Yellen Claus Saves Christmas

All Eyes Turn Toward RRP Drain

With the Treasury’s Quarterly Refunding Announcement (QRA) on Wednesday 11/1 signalling more bill issuance and less bond issuance, market fears over a spiking long-end in rates have been kicked down the road. The 10-year has already fallen 40 bps in two days, and stocks are undergoing a vicious short-covering rally.

I expect the squeeze higher in the stock market to continue into year-end.

What the QRA?

Every quarter (on or about Feb 1, May 1, Aug 1, Nov 1) the Treasury puts out there Quarterly Refunding Announcement, where they tell the market how much debt they will be issuing in the upcoming two quarters, and what the composition of that debt will be at all tenors of the curve.

On Wednesday, 11/1, the Treasury released the latest QRA. As the United States widening fiscal deficits have been well documented, and there has been some shaky auctions and heightened volatility in the bond market as of late, the market was especially keen to digest this latest announcement.

The expectation was that the Treasury was going to stick their announced policy of targeting 15%-20% of outstanding debt to be in bills, with the remainder in notes and bonds (i.e. “coupons”). And because the Treasury relied heavily on bill issuance the past two quarters to rapidly refill the Treasury General Account (TGA), in the upcoming two quarters they were going to have to moderate the pace of bill issuance in favor of coupon issuance to adhere to their stated policy goals.

Well, the Treasury blinked.

After intitially guiding $396-$460bn in coupon issuance next quarter, the Treasury stated that it will only be issuing $348bn in coupons.

The key sentence in the TBAC report was: “The Committee supported meaningful deviation from the historical recommendation for 15-20% T-Bill share.”

So, the Treasury is going against stated policy in order to limit coupon issuance in favor of bill issuance. This is doubly true since the Treasury also has the mandate to fund the government at the least cost to the tax payer, meaning they are meant to prioritize issuance at the lowest part of the curve, which is currently the 10-30 year tenor. Instead, they are issuing bills at 5.5% instead of issuing bonds at 5% (now 4.5%).

The question is, why? And, most importantly, what are the implications?

One possible reason is they suspect the market can’t absorb the increase in coupon issuance. Meaning, yields would continue to rocket higher/bond prices continue to crater in a disorderly fashion has they gone ahead and stuck to their previously issued guidance. I find this to be the most likely explanation.

If that’s the case, this latest change in policy is simply delaying judgement day, as eventually the government will have to increase coupon issuance, or else face even-more-rapidly spiraling fiscal deficits because they are opting to borrow at 5.5% instead of 4.5%.

Another, perhaps more cynical but also plausible reason would be this was a political choice, and the Treasury and Administration prefers to try to goose the economy heading into next year’s Presidential election instead of risking derailing it. This is achieved by tapping the RRP (discussed here) to fund the government and provide liquidity to the financial markets via bill issuance, as opposed to competing for private market investment via coupon issuance.

Whether that was the primary motivation or not, it seems that will be the likely outcome given the policy decisions communicated this week.

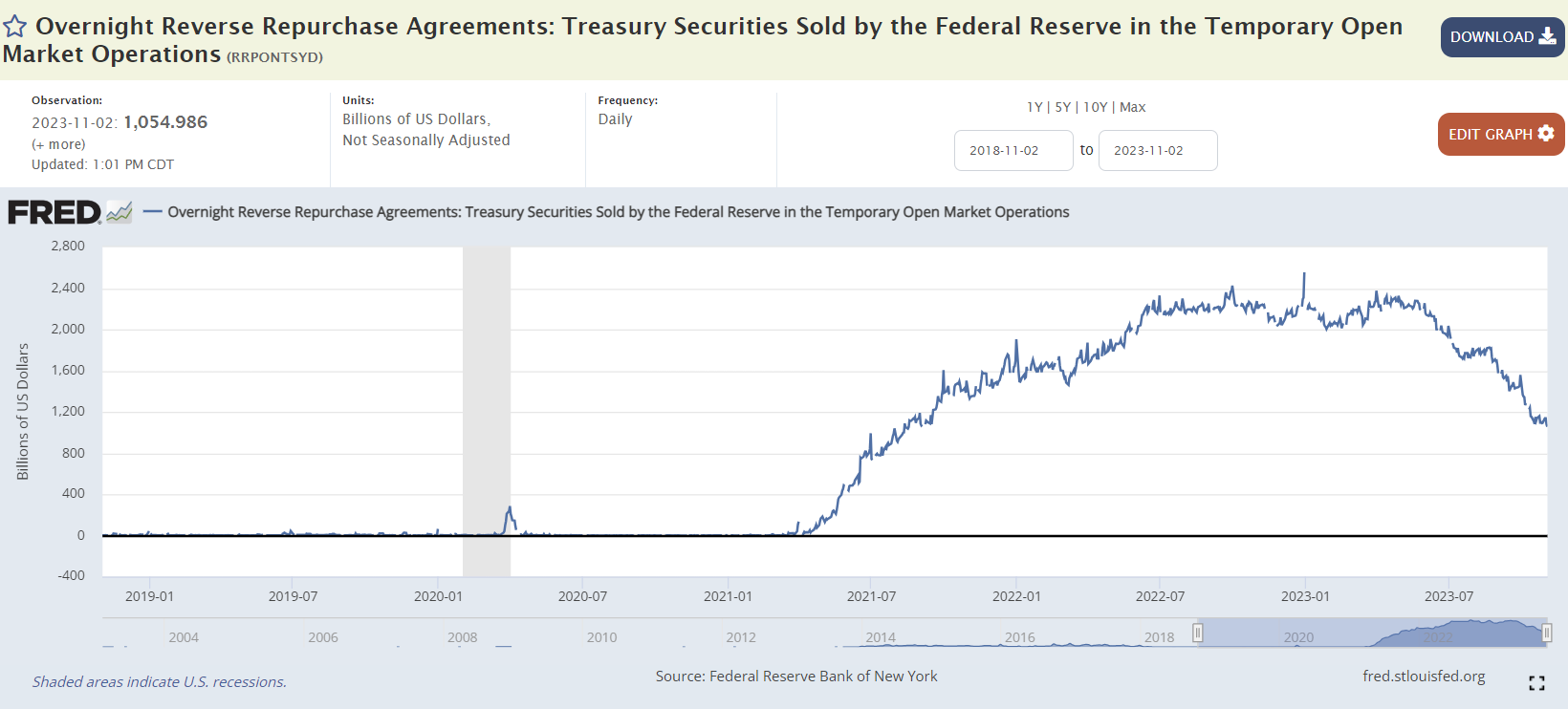

As such, I’m turning my attention to the draining of the RRP as the next big, visible risk factor on the horizon for financial markets.

This is the last remaining slush fund for the US economy, and it has just over a trillion dollars left in it, down from a high of $2.5 trillion to start the year.

As the Treasury issues bills over the coming two quarters, the money to fund the bills will come from this trillion dollar pool of assets. This should act as a sugar high for the economy, as reserves pour back onto bank balance sheets and money enters the private sector via the interest rate on bills and possibly increased bank lending.

At this point, I suspect only when it is drained will come the crash after the high.

As such, I think the set-up now favors risk assets heading into year-end and into 2024.

As of Wednesday’s announcement I have covered all my equity puts, cut a significant portion of my short book, and increased equity longs. I’ll choose to hedge with cash earning 5.5% as opposed to outright market put options.

Risks to the Outlook

As always, I could be completely wrong. I was wrong coming into the QRA, thinking the Treasury was bite the bullet and stick to their policy in the face of increasing bond market volatility. Instead, they chose to delay the economic pain.

The primary risk to the above thesis that I see is that, despite coming in way below expectations, $348 billion is still a lot of coupon issuance. It is possible that the market simply can’t even absorb this amount, and after a quick reprieve bond yields start grinding higher again.

Another risk is if and when the market turns its attention back towards inflation. The irony of the Treasury’s policy decision is that it flies in the face of the Fed’s fight against inflation. By acting in a way that brings down bond yields, the Treasury has conducted monetary policy and been stimulative to the economy. Should inflation perk back up in a meaningful way, it could cause bond yields to rise back to all-time highs much faster than I anticipate.

A third, related, risk is oil spiking higher. This could be due to war breaking out in the middle east and/or Russia choosing to weaponize energy this winter by cutting production/exports. This would simultanesouly stoke inflation and tighten economic conditions.

Finally, I expect the “higher for longer” interest rate regime we now find ourselves in to prove challenging for the banking sector, after an intial boost to reserves coming from the draining of the RRP. Also, the Bank Term Funding Program (BTFP) is set to expire in March 2024. I think it ultimately gets extended and the temporary band aid becomes permanent, but if it doesn’t, banks will probably need to resume selling treasury bonds to shore up their balance sheets, which will be another source of pressure on the bond market.

In sum, I think the risks to the equity market mainly stem from 10-30 year rates pulling a gotcha and resuming their upward trend. As such, I think an opportunity to short bonds will re-present itself over the coming two quarters and could be a good hedge against being long stocks. I also think a good opportunity re-short regional banks will re-present itself.

Finally, I think oil presents a good all-weather hedge to being long both bonds and stocks at the moment, and will be looking to increase my allocation over the coming months.

But for now, it feels like it’s up only for stocks and bonds into year-end.

Yellen Claus saved Christmas.