MicroStrategy Is A Bitcoin Bank

MicroStrategy Is A Bitcoin Bank

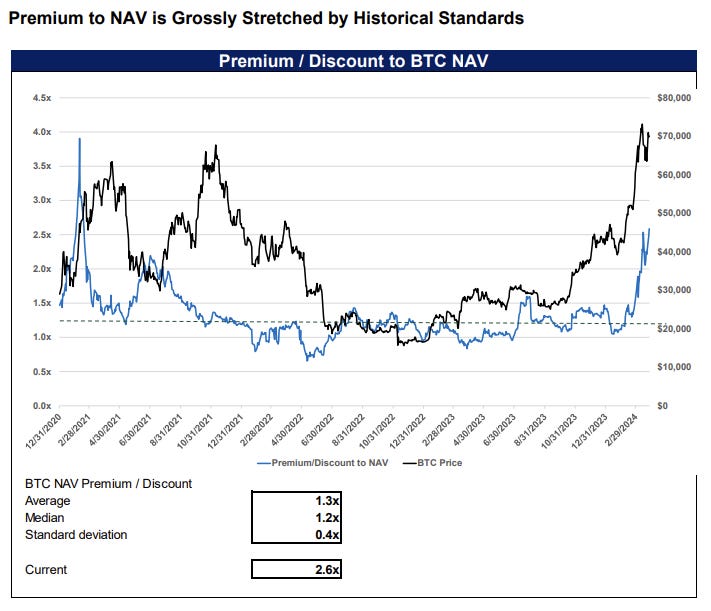

At 2.6x, MicroStrategy’s equity premium is exceptionally high. Since the beginning of 2021, the premium has been 2.0x or below on 94% of trading days. The historical average is 1.3x. …

… While we concede that some equity value premium to spot can be argued, none of them support the current 160%.

— Kerrisdale Capital report on MicroStrategy, March 28, 20241

This got me thinking: what is the appropriate premium(discount) to apply to MSTR’s Net Asset Value (NAV), i.e. their bitcoin value per share?

AKA, 'tangible book' value per share?

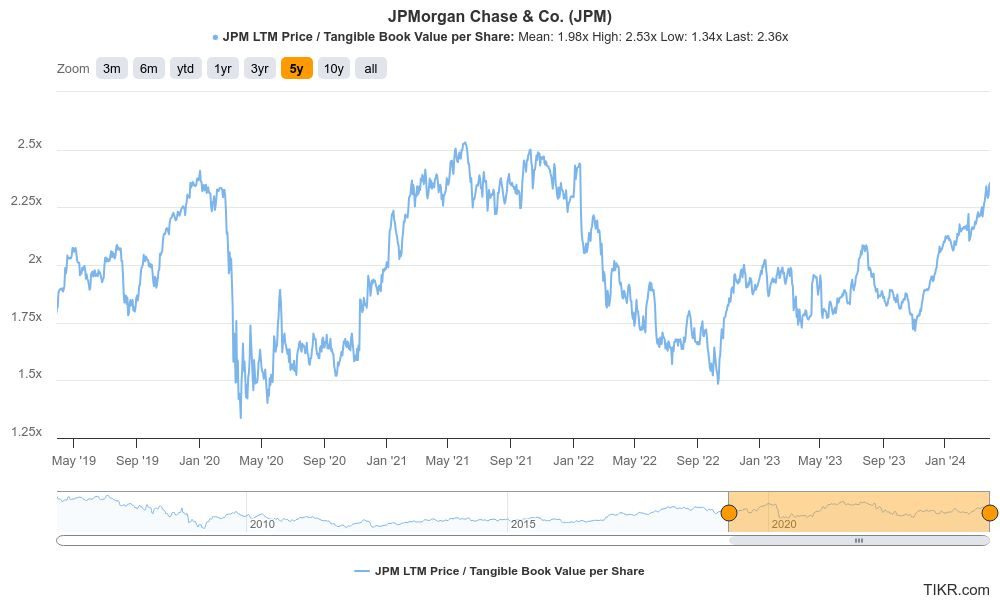

If the market is paying 2.4x tangible book for JPM, is 2.6x 'tangible book' for MSTR really that “exceptionally high?”

Calculating MicroStrategy’s Book Value Per Share

If we want to know what MSTR’s book value per share is we need to know the a) book value and b) number of shares.

For a discussion of book value, please see the footnotes,2 but for now, for clarity, assume MSTR’s book value = tangible book value = NAV = value of their bitcoin holdings.

Since MSTR’s bitcoin holdings account for the vast, vast majority of their book value, for this analysis we will simply calculate their book value as the value of their bitcoin holdings.

For completeness (as per the graphic from Kerrisdale below), they do have $3.6 billion in debt, of which $2.5 billion is currently in-the-money convertible notes.

Kerrisdale adjusts their calculation of diluted shares for the in-the-money converts and subtracts the remaining ~$1.1 billion in net debt from their calculation of NAV (i.e., book value).

For ease of consistent comparison across time, we’re simply going to assume 1) all of the converts as in-the-money (in-the-money means the debt will convert to equity), 2) full dilution from all the converts and 3) zero debt in my calculation of book value. We are also going to assign no value to the software operating business, which Kerrisdale values at $1.25 billion.

These numbers can be quibbled over, and so we’re conservatively going to simply exclude both the $450 million net debt and the ~$1.25 billion EV software business, the net of which is immaterial to $15 billion in bitcoin holdings that often fluctuates by +-5% a day.

This actually results in a lower calculation of BTC holdings per fully diluted share than Kerrisdale comes up with (conservative!), so hopefully nobody has any problems with my methodology :)3

Here is the current snapshot, using 4/1/24 closing prices:

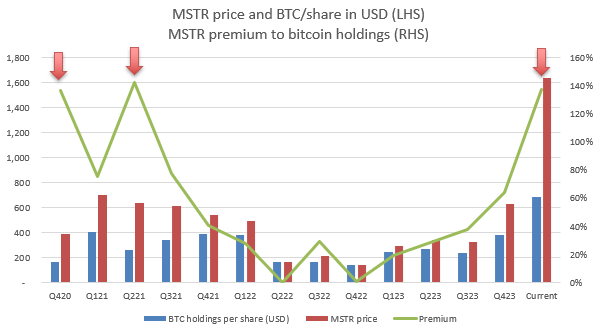

MSTR has 0.0099 bitcoin per share, equal to $689 per share.

Here are the Q4 snapshots since MSTR adopted their bitcoin strategy in Q3 2020, so you can see how BTC share has grown over time (fully diluted shares are taken from page 29 of the Q4 2023 earnings presentation; current shares have been adjusted for the two, recent convertible note offerings):

MSTR is currently trading at ~2.4x book, a richness it has only achieved in Q4 2020 and Q2 2021 as shown below (the Kerrisdale chart at the top is a more granular look at this, and shows that P/B got as high as 3.9x in early 2021):

MSTR has grown BTC/share from 0.0057 in Q4 2020 to 0.0099 today, an 18.9% CAGR (compound annual growth rate).

(I will note here that Kerrisdale disagrees with this CAGR as they, as mentioned, only assume dilution from in-the-money converts. Nonetheless, they still show 0.0108 BTC/share, which is actually more than the 0.0099 BTC/share I calculate.)

Note that this 18.9% book value per share CAGR is in BTC, not USD.

Saylor is compounding the amount of bitcoin you own per share of MSTR at 18.9% annually.

Imagine you have a piggy bank with 1 bitcoin in it, and next year 0.189 bitcoins get added to the piggy bank without you doing anything, and the year after that 0.225 bitcoins get added , and the next 0.267 bitcoins … and so on.4

How many bitcoins would someone need to pay you today to get you to relinquish your bitcoin piggy bank?

Because right now the market is offering you 2.4 bitcoins for your bitcoin piggy bank.

Comping MicroStrategy to Banks

At the top, we teased that MSTR’s premium to NAV might not be so rich if instead of thinking of the valuation in terms of a premium to NAV, you thought of the valuation in terms of a price/tangible book multiple, like you would a bank.

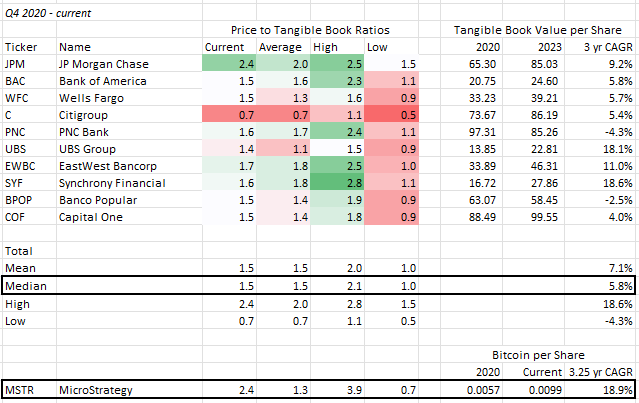

Below is a comp table of 10 banks, including the four Too Big To Fails and a sampling of six more that generally run the gamut in terms of size, and that I consider to be relatively well run.

JP Morgan is generally considered to be the gold standard, and sports the highest current valuation on Price/Tangible Book with a 2.4x multiple (top left of table). Since Q4 2020 they’ve grown tangible book value per share at 9.2% annually (top right), faster than peers, but not the fastest in our table.

We choose Q4 2020 as a starting point since MicroStrategy embarked on their bitcoin strategy in Q3 2020. So MSTR was a full two quarters into acquiring bitcoin as of their Q4 2020 report, by which time they had acquired 70,469 bitcoins (a full 32.9% of their current stack) or 0.0057 BTC/share.

Thus, our bitcoin per share CAGR for MSTR is not distorted by starting from a low base.

If the Best Bank on Earth™ is compounding book value at 9.2% annually and the market thinks that’s worth 2.4x book today, then is it crazy that the only Bitcoin Bank™ — the only publicly traded equity with a stated or revealed strategy of increasing bitcoin per share — compounding bitcoin per share at 18.9% annually, is also trading at 2.4x book?

Idk? I don’t think so?

So, to answer the question, what is the right price/book multiple to value MSTR at?

I have no idea.

But, when Kerrisdale or others say that a 160% premium to NAV (2.6x book value) is wildin’, I think their reasoning by analogy is flawed.

In my opinion, the proper analogy is not to consider MSTR’s premium or discount to NAV like you might for a (previously) closed-end fund like GBTC.

The proper analogy is to consider MSTR’s price/book multiple like you might for a bank that was accreting book value per share over time.

MicroStrategy is a Bitcoin Bank™.

As of 4/1 close, MSTR is down -14.7% from its 3/27 closing price of $1,919.16, the day before Kerrisdale published their long bitcoin/short MSTR pair trade thesis. Over the same time period, bitcoin is up 1%, and MSTR’s premium to NAV has fallen from 2.6x to 2.4x.

Book value = NAV (net asset value). It’s the balance sheet value of assets net of liabilities (thus, 'net' asset value). Also known as shareholder’s equity.

'Tangible' book value simply excludes goodwill and other intangible assets, of which MSTR has none, so we don’t need to worry about distinguishing between 'book' value and 'tangible book' value when speaking about MSTR.

Tangible book is generally considered to be the liquidation value of a bank, i.e. if all assets were sold, all liabilities paid and the difference was returned to shareholders. For MSTR, this would mean selling all of their bitcoin at the current market price, paying off their debt and returning the leftovers to shareholders.

But if you do, leave me a note in the comments and I’m happy to share my calculations and discuss further if you want.

Yes, I know that MSTR won’t be able to compound bitcoin per share at 18.9% forever.