Voyager Files for Chapter 11 Bankruptcy

What it Means for Customers

First of all, I have major egg on my face on this one.

I feel terrible and embarrassed that I pitched Voyager and their 9% rewards on USDC very publicly over the past couple of months. I regret labeling USDC as risk-free* even though I clearly explained (I hope) that risk-free* was meant to describe the USD:USDC peg, and there was still counterparty risk in dealing with Voyager (just as there is with any counterparty) which I covered extensively here.

Indeed, bitcoin was created in 2009 in the wake of the Global Financial Crisis in part to solve for the notion of counterparty risk as a digital bearer asset that is no one else’s liability.

Not your keys, not your coins. We are viscerally learning the meaning of the phrase in this bear market.

Clearly my evaluation of Voyager counterparty risk turned out to be inaccurate, and I continue to contend that they misled investors and customers by stating in this June 14 press release that they do “not participate in DeFi lending activities, algorithmic stablecoin staking and lending, or derivative assets, such as stETH” and were “well capitalized and in a good position to weather this market cycle and protect customer assets” when they had a $650 million loan outstanding to troubled crypto hedge fund Three Arrows Capital (3AC), which was known at the time to be engaging in these activities.

Finally, when news broke last week of Voyager’s exposure to 3AC, I wrote about steps Voyager customers could take to limit their exposure and protect their assets here, including getting all crypto off the platform or converted to USD, which is held on behalf of Voyager customers at Metropolitan Bank and is FDIC insured up to $250k.

I was able to do this and hope my readers (and everyone!) were too, although I still have a sizable (5 figures) amount of USD on the Voyager platform and currently illiquid as Voyager has temporarily suspended all withdrawals, as well as a few hundred dollars worth of crypto rewards (currently held in crypto) that paid on July 1. So, I’m feeling some financial pain and uncertainty here, too.

That all said, what’s happened since my last post on June 22, and what to do moving forward?

Friday, July 1: Voyager Temporarily Suspends All Trading, Deposits and Withdrawals

Press release here.

At the time, my best guess was that Voyager was urgently working on a deal similar to the one BlockFi announced with FTX earlier that same day, in which BlockFi received an increased $400 million revolver (up from previously announced $250 million) and an option for FTX to acquire at a variable price of up to $240 million. This appears to be an opportunistic and great deal for FTX, as they get to lend to the distressed lender and if they make it through the current market they have an option to purchase the whole business for less than the $350 million BlockFi raised in March 2021 at a $3 billion valuation. I don’t know all the details, but presumably this deal effectively wipes out all BlockFi equity holders and speculation is that BlockFi had to take it as the only deal which offered debt subordinate to customer assets. In any event, BlockFi customers retained liquidity to their crypto assets throughout and BlockFi is continuing normal operations, including actually raising the interest rates offered on major assets such as BTC and ETH.

My base case was that a similar deal for Voyager was being worked on, but when it became clear they wouldn’t be able to hammer it out before the holiday weekend Voyager froze customer assets to ensure they’d survive the weekend.

To be clear, that’s me speculating. Who knows what the actual truth is.

Despite what has transpired since as we’ll cover below, including Voyager filing for Chapter 11 bankruptcy, I believe a “white knight” acquirer situation similar to BlockFi’s still represents the best chance for Voyager customers to realize a full recovery of their crypto assets.

4th of July Weekend: Speculation Begins That Customer’s USD on Voyager is Not Actually FDIC Insured as Advertised

This is when I had to excuse myself from the lawn games and the hot dogs in my stomach began to turn.

Frances Coppola of 76k Twitter followers speculated on her blog that something was amiss with Voyager’s claims of FDIC insurance through their partner bank Metropolitan Bank and their restricting customer withdrawals of USD (spoiler: this appears to me to have been addressed in Voyager’s subsequent statement on Chapter 11 restructuring and it seems that customer USD deposits are indeed safe, and FDIC insured, with Metropolitan Bank and will available for customers to withdraw shortly).

The relevant part of the Voyager User Agreement is:

5. Account Funding; Regulatory Treatment

(A) Customer Cash. Customer understands and acknowledges that Customer may arrange to deposit United States Dollars (“USD” or “Cash”) into the Account. Cash deposited into the Customer’s Account is maintained in an omnibus account at Metropolitan Commercial Bank (the “Bank”), which is a member of the Federal Deposit Insurance Corporation (“FDIC”). Voyager maintains an agreement with the Bank whereby the Bank provides all services associated with the movement of and holding of USD in connection with the provision of each Account. Therefore, each Customer is a customer of the Bank. All U.S. regulatory obligations associated with the movement of, and holding of, USD in connection with each Account are the responsibility of the Bank. For purposes of clarity, any services pertaining to the movement of, and holding of, USD are not provided by Voyager or its Affiliates. Cash in the Account is insured up to $250,000 per depositor by the FDIC in the event the Bank fails if specific insurance deposit requirements are met. FDIC insurance does not protect against the failure of Voyager or any Custodian (as defined below) or malfeasance by any Voyager or Custodian employee. Voyager is not a member of the Financial Industry Regulatory Authority, Inc. (“FINRA”) or the Securities Investor Protection Corporation (“SIPC”), and therefore Cash is not SIPC-protected.

Now, this seems to pretty clearly stipulate Metropolitan Bank having full control and custody of USD deposits and FDIC insurance for those deposits, but I believe the confusion and fear arose out of two points: 1) Confusion: customer USD deposits not being FDIC insured against Voyager insolvency, only against Metropolitan Bank insolvency and 2) Fear: if Metropolitan Bank does have full control and custody of USD deposits and “provides all services associated with the movement of and holding of USD” then how could Voyager suspend USD withdrawals?

Let’s take them one at a time. First, on the point of Voyager not being FDIC insured but rather Metropolitan Bank, that makes sense and is what you would expect. Hence the partnership in the first place. I think there was confusion around this point but this was always clear and represented. You want the entity where your USD deposits are ultimately held to be FDIC insured.

Metropolitan Bank put out a statement specifically addressing the Voyager situation that was non-reassuring legalese, but didn’t actually say anything alarming or to the contrary of what one would expect, in my opinion.

However, where the legitimate fear and questions begin is, if customer USD deposits are all held at the Bank as stipulated in the user agreement, then how could and why would Voyager suspend all USD withdrawals?

I don’t have a good answer for this, and this is where fear of outright fraud creep in.

For example, one possible explanation would be that Voyager was expropriating customer USD deposits and not actually holding them all at the Bank. If that were the case, I’d have to imagine someone would end up in jail.

(*Editor’s note: it appears the suspension of USD withdrawals may have been initiated to allow time for Voyager and MC Bank to jointly investigate fraudulent customer chargeback requests. See more below.)

One more piece of uncertainty stems from whether each Voyager customer individually is FDIC insured up to $250k, or since deposits are commingled in an omnibus account, if only that one account is insured up to $250k. I will continue to research this, but I can’t imagine it’s the latter, and in any event, it’s somewhat moot since as discussed above FDIC insurance only matters in the event of a Bank insolvency, not Voyager, and so long as Voyager was not expropriating customer USD deposits and were truly holding them at the Bank as represented, those deposits are safe and sound.

Night of July 5th: Voyager Files for Chapter 11 Bankruptcy

For those unfamiliar, Chapter 11 bankruptcy is a voluntary restructuring during which a company continues to operate and emerges a viable ongoing concern, as opposed to Chapter 7 bankruptcy which entails a complete liquidation of all company assets and repaying to creditors in order of seniority. Here’s a quick review of Chapter 11 vs. Chapter 7.

Voyager’s full press release from last night is here, but here’s the important part (emphasis mine):

The proposed Plan of Reorganization ("Plan") would, upon implementation, resume account access and return value to customers. Under this Plan, which is subject to change given ongoing discussions with other parties, and requires Court approval, customers with crypto in their account(s) will receive in exchange a combination of the crypto in their account(s), proceeds from the 3AC recovery, common shares in the newly reorganized Company, and Voyager tokens. The plan contemplates an opportunity for customers to elect the proportion of common equity and crypto they will receive, subject to certain maximum thresholds.

Customers with USD deposits in their account(s) will receive access to those funds after a reconciliation and fraud prevention process is completed with Metropolitan Commercial Bank.

In short, if you have crypto on the platform you’re probably not getting all of it back, and if you have USD on the platform you are, pending the “reconciliation and fraud prevention process” being completed with the Bank, getting all of it back.

I don’t know why a reconciliation and fraud prevention process needs to be done and what that entails, nor how long it takes to complete. But, regardless, it seems, for the moment, that your USD is safe with Voyager and always was.

(*Editor’s note: I’ve learned from Matt Levine’s just published article that apparently customers are calling their banks and saying that their ACH transfers to Voyager were fraudulent and are attempting to get them reversed. This means, for example, customers could have transferred $40k from their bank to Voyager, bought 1 BTC for $40k which is now worth $20k and frozen, and get back $40k by claiming the initial ACH transaction was fraudulent, transferring the intervening price risk from themselves to Voyager’s other customers. Voyager is seeking to prohibit MC Bank from honoring chargeback requests for a 60 day period from the freeze date July 1 while they work together to determine if such requests are legitimate or fraudulent. Per this information, it seems Voyager customers who are rightful owners of USD could have their assets frozen for 60 days from July 1, or until September 1. See screenshot below.)

Unfortunately we can’t say the same for crypto assets, including USDC. While it’s possible customers are made whole, as part of what they recover is dependent on what Voyager recovers from 3AC, it seems unlikely. Rather, customers will given a mix of crypto, common stock in the newly restructured entity, and Voyager tokens as compensation.

Voyager stock has been suspended from trading as of this morning.

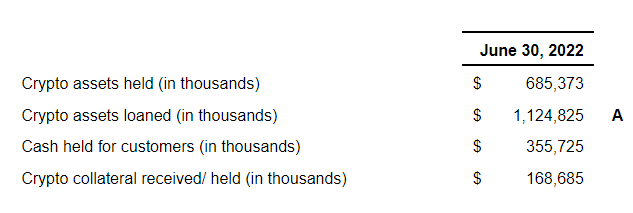

The latest press release indicates that Voyager has $1.3 billion of crypto assets held on the platform, up from $685 million reported in the July 1 press release. That’s in addition to $350 million of USD held for customers at the Bank and $650 million of claims against 3AC, which might amount to nothing. They also have $110 million in liquidity to continue operations during the restructuring, for things like paying employees.

The July 1 press release that indicated $685 million in crypto assets held for customers also indicated $1.1 billion in crypto assets loaned. Presumably the crypto assets loaned balance has decreased commensurate with the increase to $1.3 billion in crypto assets held, which would represent a recovery of substantially all crypto assets loaned to non-3AC counterparties and a remaining $650 million of crypto assets loaned to 3AC.

I’m not sure if this is the right way to look at it, but if you assume a $650 million shortfall on $650 million + $1.3 billion = ~$2 billion of customer crypto balances, then crypto asset owners might expect to recover approximately ~67.5 cents on the dollar (indeed as I write this, Matt Levine writes that customers might expect back 72 cents on the dollar, and I will echo his caveat that this is not investment advice!).

Typical time for a Chapter 11 proceeding to resolve is 6-24 months.

I believe Voyager could still reach an agreement with FTX, Alameda Research or someone else to be acquired and resume normal operations a la BlockFi. This represents the best chance for customers to realize a full recovery of their crypto assets on the platform, and I have to believe these talks are ongoing.

Other Options for Yield on Cash

Back to where we all started. If you got yourself into this mess like I did by using options to replace equity exposure and searching for a high-yielding option on cash to juice your returns, there are still some options for a return on USD. I’m going to humbly refrain from suggesting anything crypto-related here and just focus on FDIC insured options for USD.

First, I’ll state that if you have no better use for the cash, you can simply reverse the trade and flip your options exposure back into equity exposure, realizing more or less a return of the premium paid for the option after backing out the change in price of the underlying. You will have paid a little bit for the time value decay of the option and will have made or lost a little money on the change in implied volatility of the underlying asset since your purchase date.

Next, I’ll again mention Series I Savings Bonds, which are currently yielding 9.62%. The maximum an individual can invest in these bonds is $10,000 per annum.

Finally, I’ll mention the Marcus Online Savings Account by Goldman Sachs, currently yielding 1.20%. The yield on this account should increase as the Fed Funds rate increases. I’ve been a customer of Marcus before and recommend. It’s no 9%, but it’s something if you need a place to park your liquid savings.

Disclaimer: nothing published in this newsletter is investment or financial advice. The author may be long or short any of the securities or assets discussed at any time before or after publishing.