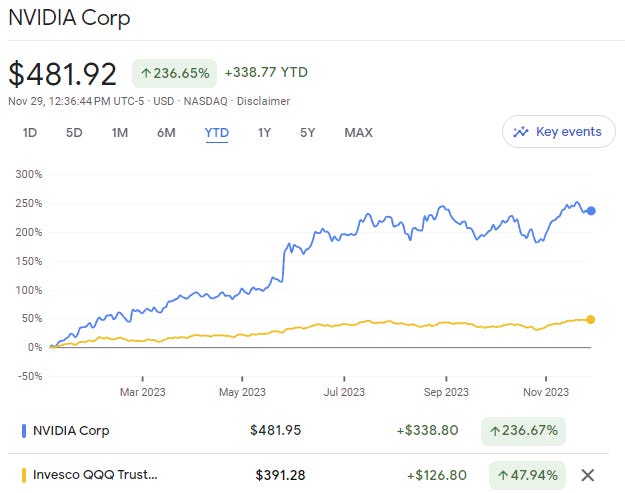

After a pretty brutal year for tech stocks in 2022, I was caught a bit off-sides by the AI-fueled rally in 2023.

As I was caught-up in the narrative of the TGA refill and hedging my bets, tech exploded higher and dragged the indices up with it, led by AI poster-child NVIDIA.

NVIDIA GPUs (graphic processing units) are the chips that are best suited to processing deep learning model demands. They are the backbone to the LLMs (large language models) which serve as the foundational tech for consumer products like ChatGPT, as well as the neural nets that a company like Tesla is training to drive cars — i.e. “real world AI.”

As the NVDA 0.00%↑ stock price rocketed higher in May, peaking at 70x next twelve months (NTM) sell-side earnings estimates / 26x NTM revenues, comparisons were being drawn to dot-com era stocks of lore such as Cisco Systems and Sun Microsystems.

I wasn’t around then (well, I was around, but 10 years old and much more worried about how my Utah Jazz were fairing than the stock market) so I had to go back and study the period a bit closer in an effort to form an investing opinion on AI.

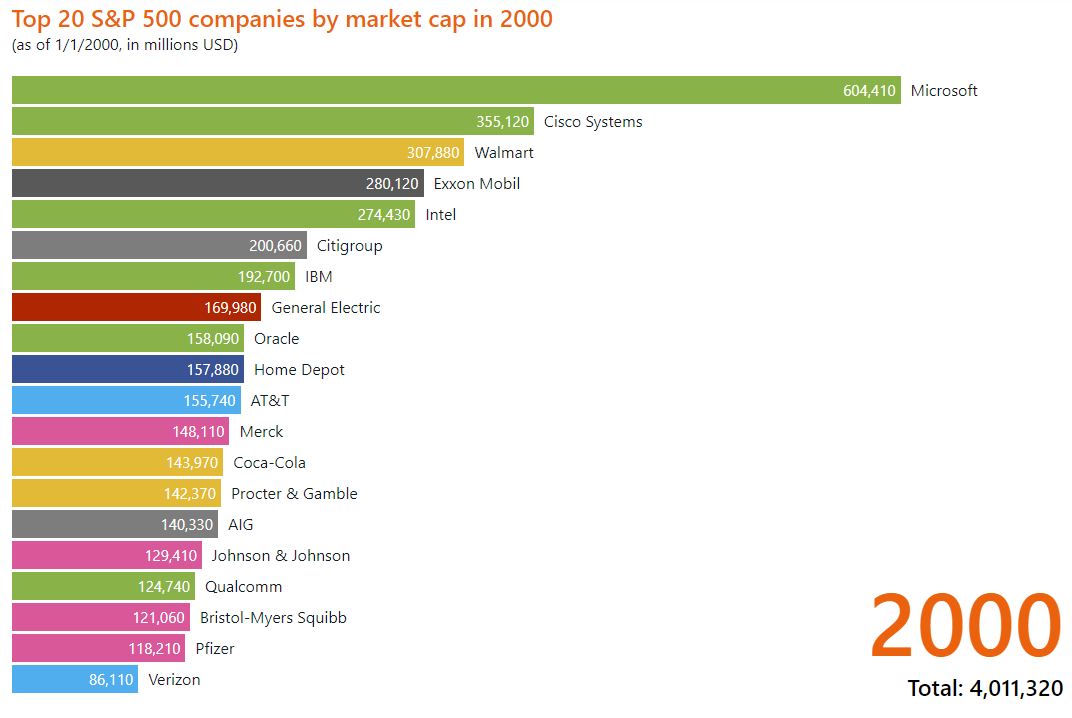

Cisco, at it’s peak in March 2000, grew to be the most valuable company in the world at a market cap of $546 billion.

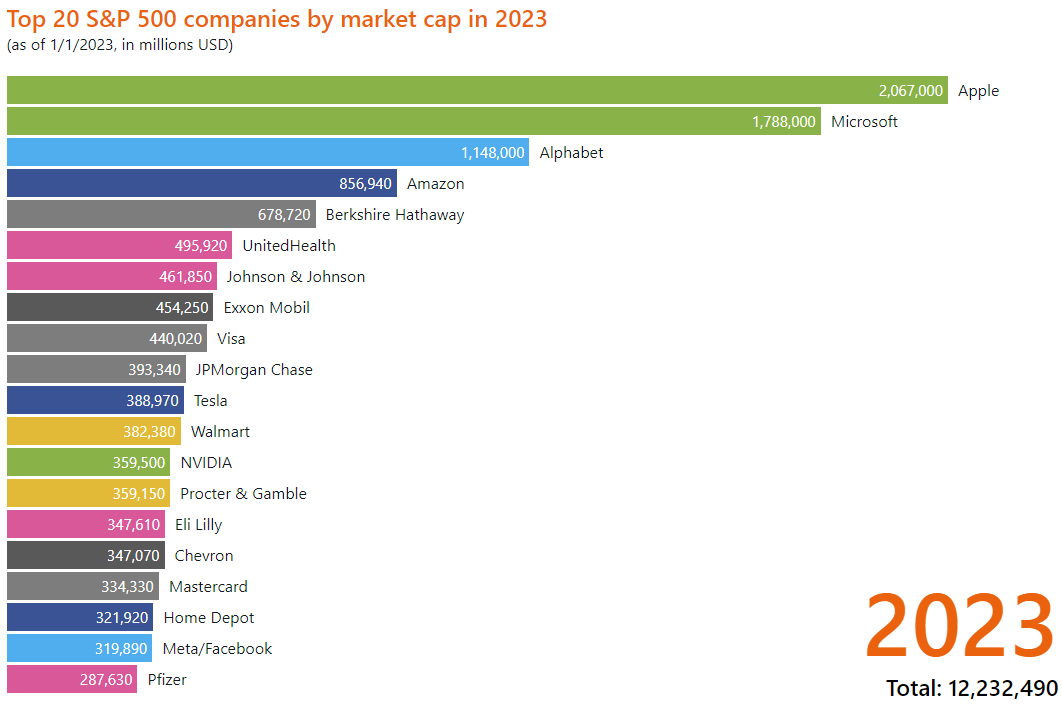

Here’s a snapshot of the largest companies in the S&P 500 as of Jan 1, 2000:

So you can see, CSCO 0.00%↑ rose from a market cap of $355 billion to $546 billion, or 54%, in less than 3 months from January to March of 2000 at the tail-end of the dot-com bubble.

Of course, we all know what happened afterwards.

The dot-com crash, which prompted Sun Microsystems CEO Bill McNealy to remark to Business Week in 2002:

At 10 times revenues, to give you a 10-year payback, I have to pay you 100% of revenues for 10 straight years in dividends. That assumes I can get that by my shareholders. That assumes I have zero cost of goods sold, which is very hard for a computer company. That assumes zero expenses, which is really hard with 39,000 employees. That assumes I pay no taxes, which is very hard. And that assumes you pay no taxes on your dividends, which is kind of illegal. And that assumes with zero R&D for the next 10 years, I can maintain the current revenue run rate. Now, having done that, would any of you like to buy my stock at $64? Do you realize how ridiculous those basic assumptions are? You don’t need any transparency. You don’t need any footnotes. What were you thinking?

I think this is an easy thing to say in hindsight. The problem is you could have said basically the same thing at the beginning of 1998 — a full 3 years into the dotcom boom — and missed a 274% return over the next two years.

When NVDA rose from $305 on 5/24 of this year, to $475 on 7/18, an increase of 56% in a little less than two months, to trade at not 10x but 26x revenues(!), the comparisons to the dot-com bubble were drawn and many predicted it would end badly for investors who joined the party late.

But you know when else Cisco went up by at least 50% in three months, before it’s final peak in March 2020 (and not counting it’s first 5 years of trading after it’s 1990 IPO)?

May - Jul 1995

Apr - Jun 1997

Sep - Nov 1998

Sep - Nov 1999

So, the questions for investors today are:

Is NVDA actually overvalued today?

What inning of the AI revolution are we in? Are we in 1995 or 2000?

My answer: AI will create one of, if not the, largest technology driven investment bubbles of all time, and we’re just getting started.

NVDA Can Be The Most Valuable Company In The World

There is a good chance that NVDA’s products are the bottleneck to achieving artificial general intelligence (AGI), for many years to come.

If this is the case, I see no reason why NVDA can’t become the largest company in the world before this AI investment supercycle is done and dusted.

In fact, history might suggest this is indeed the company’s destiny.

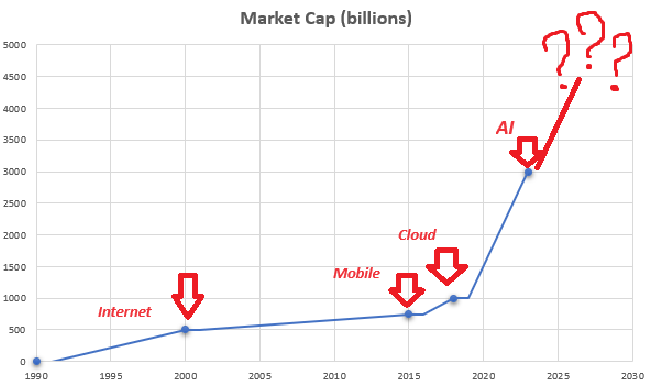

We’ve lived through three prior technology driven investment supercycles in recent history, and are currently living through a fourth:

Internet

Mobile

Cloud

AI

In each previous cycle, the preeminent infrastructure/hardware layer provider for the new technology has become the most valuable company in the world.

We already covered Cisco, the networking hardware and telecommunications equipment provider that serves as the backbone of the internet, becoming the world’s most valuable company at a peak market cap of $546 billion in 2000 at the height of the internet supercycle/dot-com bubble.

The mobile supercycle began in earnest with the introduction of the iPhone in 2007. At the time, Exxon Mobil and General Electric were the most valuable companies and Apple was nowhere to be found in the top 20.

By 2012, Apple had surpassed Exxon to become the world’s most valuable company.

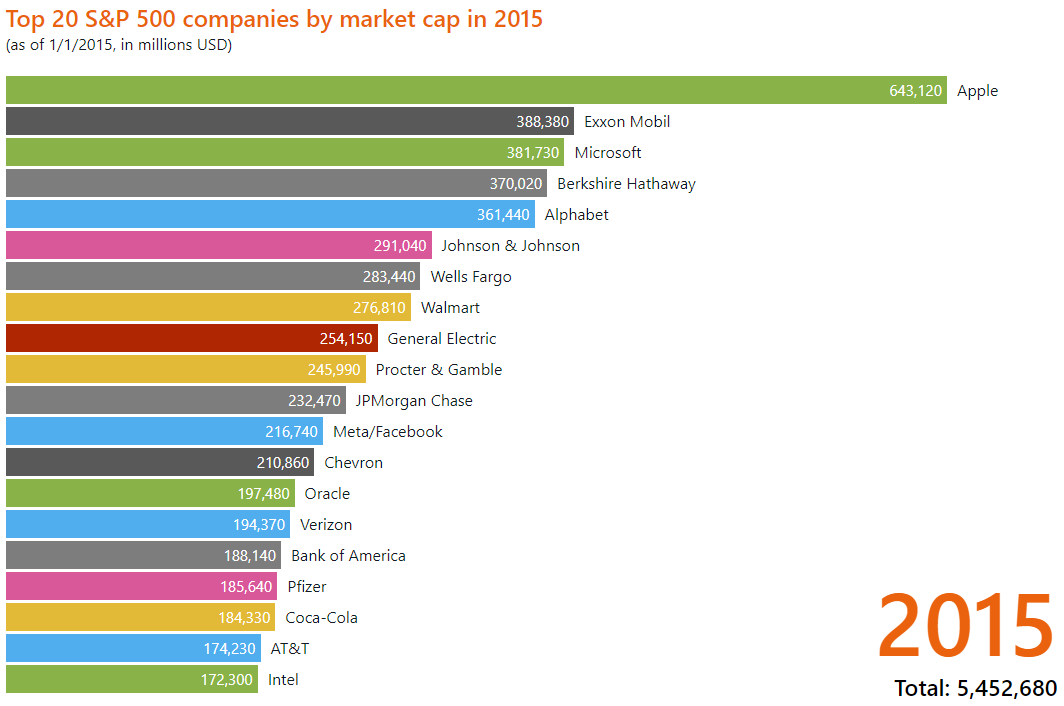

By 2015 it’s lead was dominant:

Notice that Amazon is not found in the top 20 in 2015.

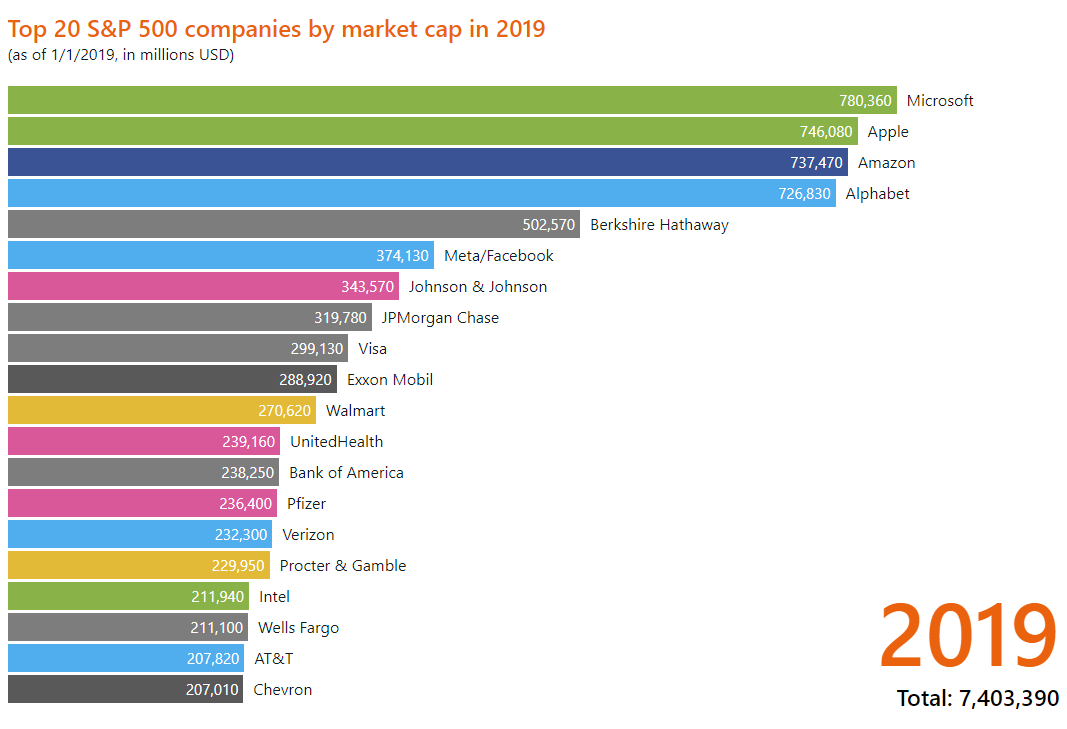

Overlapping with the mobile supercycle was the cloud supercycle, during which Amazon became the most valuable company on Earth on the back of AWS, the first public cloud:

This chart shows MSFT as top dog on 1/1/2019; by 1/7/2019 AMZN would surpass them with a market cap of $797 billion (it had previously topped $1 trillion, but MSFT was still more valuable at the time).

But what is striking to me about this graphic is it shows the three major public cloud providers (AMZN, MSFT, GOOG) head and shoulders above the rest, alongside the winner of the mobile supercycle.

And now, while we’re still in the middle of the cloud supercycle, and AAPL actually remains as the most valuable company in the world, we are at the very beginning of the AI supercycle.

Notice how NVDA was 13th on the list on Jan 1 of this year, about a month after OpenAI’s consumer product ChatGPT introduced the world to AI at scale in November 2022.

Today, they are fifth (Alphabet Class A and Class C need to be combined):

And to become the biggest, NVDA has a ways to go. AAPL’s market cap currently sits at ~$3 trillion; NVDA $1.2 trillion. NVDA would likely need to achieve at least a 3x increase in stock price to challenge Apple for world’s most valuable company, but history shows it can be done when a new tech-driven investment supercycle rises to the fore.

So to recap:

Internet: Cisco peaks at ~$500 billion in 2000

Mobile: Apple reaches ~$750 billion in 2015

Cloud: Amazon reaches $1 trillion in 2018

Today: Apple reaches $3 trillion in 2023

AI: ???

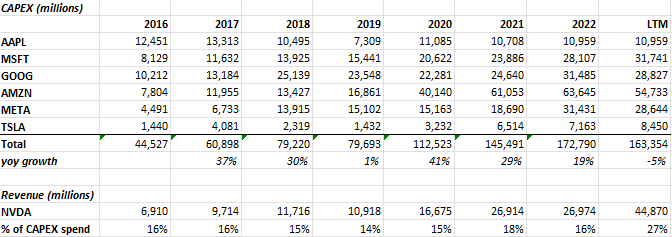

And if you doubt there is actually an investment boom happening, here is the CAPEX for the Mag 7 ex NVDA over the past 7 years (I don’t include NVDA because the whole point is that much of the other company’s spend is on NVDA chips — their spend = NVDA’s revenue):

The six largest tech companies are now investing upwards of $160 billion a year in capex, and much of that is expanding data centers, increasing cloud capacity and acquiring as many NVIDIA GPUs as they can.

On top of this, we are at the very start of a venture capital funded AI boom.

Just how in the last venture capital cycle all the venture dollars went straight to Amazon to buy cloud computing capacity to host software applications, in this cycle all the venture dollars are going to go straight to NVIDIA to buy GPUs to train AI models.

This has only barely begun.

Bubbles Get A Bad Rap

First, a new invention is greeted with skepticism from incumbent technology and potential new investors. That skepticism is gradually replaced with enthusiasm, as businessmen come to appreciate the sales potential of the new technology. Soon, new entrants are flocking to the market, and venture capital funding is made available. Companies are started; almost all do well (in terms of share price) in the market on a tidal wave of enthusiasm. So far, so good; but as the technology begins to mature, a sense of realism sets in. Inevitably, for some, cash runs out. Companies begin to fold, only the strong survive and naive investors lose money in the huge rationalization. Pessimism begins to pervade the marketplace and stock prices fall across the board. Eventually, the market stabilizes.

This same pattern occurred with the development of the railroads, electric light, oil, the telephone, the automobile, the radio, the semiconductor.

— Alasdair Nairn, Engines That Move Markets

In the investment context, the term “bubble” has a negative connotation. It is used to describe the stupidity that takes place at the peak of a mania, which always proceeds a crash, which ruins countless lives.

But I’d argue bubbles are a healthy and necessary ingredient for technological innovation and progress. They provide the (excess) capital for investing in emerging technologies and giving them best chance of realizing their full potential.

They are also where all the money is made in the stock market.

Pessimists sound smart, optimists make money.

So, if you embrace the virtue of bubbles, or at least acknowledge that they are an inevitable and recurring part of financial markets, the question for the investor becomes how to make money from them.

How To Play The Coming AI Bubble

Nothing below is advice. Everyone’s investment goals and risk tolerance is different. Please do your own due diligence.

As discussed, the hardware layer typically leads the bubble.

You need the infrastructure to support the emerging technology before new and useful tools and applications can be built.

Hardware is the fertile soil and the seed.

Applications are the fruit.

The preeminent hardware company supporting the AI revolution is likely to be NVIDIA. If it’s not them, it will likely be another semiconductor company that is able to leapfrog their tech.

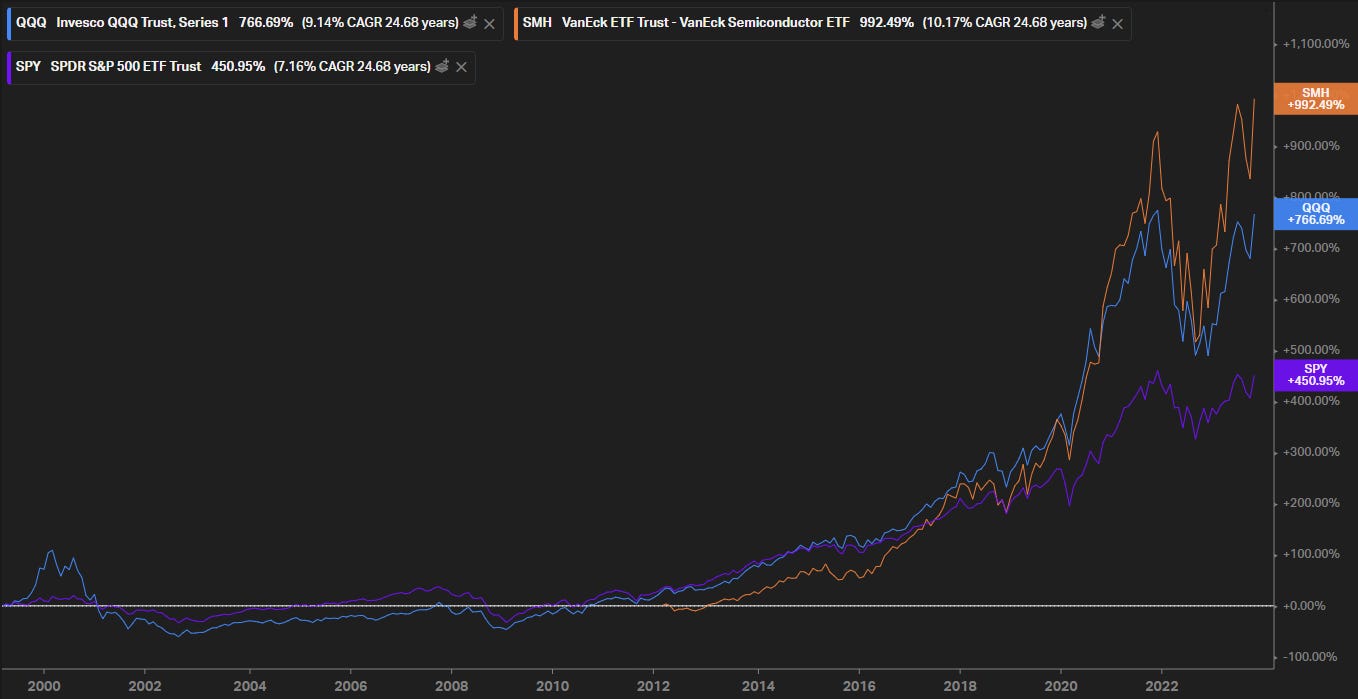

As such, I think all investors should consider maintaining at least index exposure to NVDA specifically and the semiconductor sub-sector generally within their public equity allocation, and probably seek to be at least a little overweight.

For myself, for now I’m expressing this through owning SMH VanEck Semiconductor ETF — which includes NVDA and TSM as it’s top two weights — via the ETF and June 2024 OTM call options.

Eventually, AI will power enterprise and consumer products that will accrue even more value than the hardware layer. This is the application layer.

The application layer to the dotcom bubble was Apple, Google, Facebook and Amazon.

They didn’t grow into the most valuable companies in the world until the mid 2010s, but eventually they surpassed their hardware predecessors.

I think it is way too early to know what applications will come out of the AI boom, but here are a few places I’m keenly watching along with the companies/funds I think most likely to benefit:

Self-driving cars (Tesla)

Enterprise/Government software productivity tools (Microsoft, Google, Palantir, Amazon)

AI agents (WhatsApp, OpenAI)

Humanoid robots (Tesla)

Healthcare tech (ARKG)

The above list relates to the potential for AI to enable novel, revenue generating consumer and enterprise products.

What will happen even sooner than that is a reduction in costs.

ByteDance employs 40,000 content moderators. With AI they plan on reducing that number by 90% over the next year.

This isn’t something to fear (job loss). This is something to celebrate. AI agents will free up human energy to pursue more productive and fulfilling tasks.

If you read all this and think “why don’t I just go buy QQQ then and call it a day?” you’re not wrong.

The overarching point is, as we head into what I increasingly think is likely to be the biggest tech-driven investment “bubble” we’ve ever seen, I think you want to be overweight tech generally and semiconductors specifically, as has been the case for the last 25 years:

I will also mention here I am short a small amount of Google against my “long AI” positions. I find that I have almost entirely replaced my search activity with ChatGPT queries and talk with others that report the same. It seems to me like Google, as the dominant incumbent, has the most to lose in a paradigm shift for how we query and retrieve information.

I think it’s likely that Google like has ChatGPT-level AI capabilities right now, ready to ship, but is caught in a classic innovator’s dilemma because to the extent the new product is successful, it will destroy their existing search business.

As with any technological revolution, there will be losers as well as winners.

How To Time The Coming AI Bubble

Even more important than selecting the fastest surfboard will be simply making sure to catch the wave, and to get off without crashing if possible.

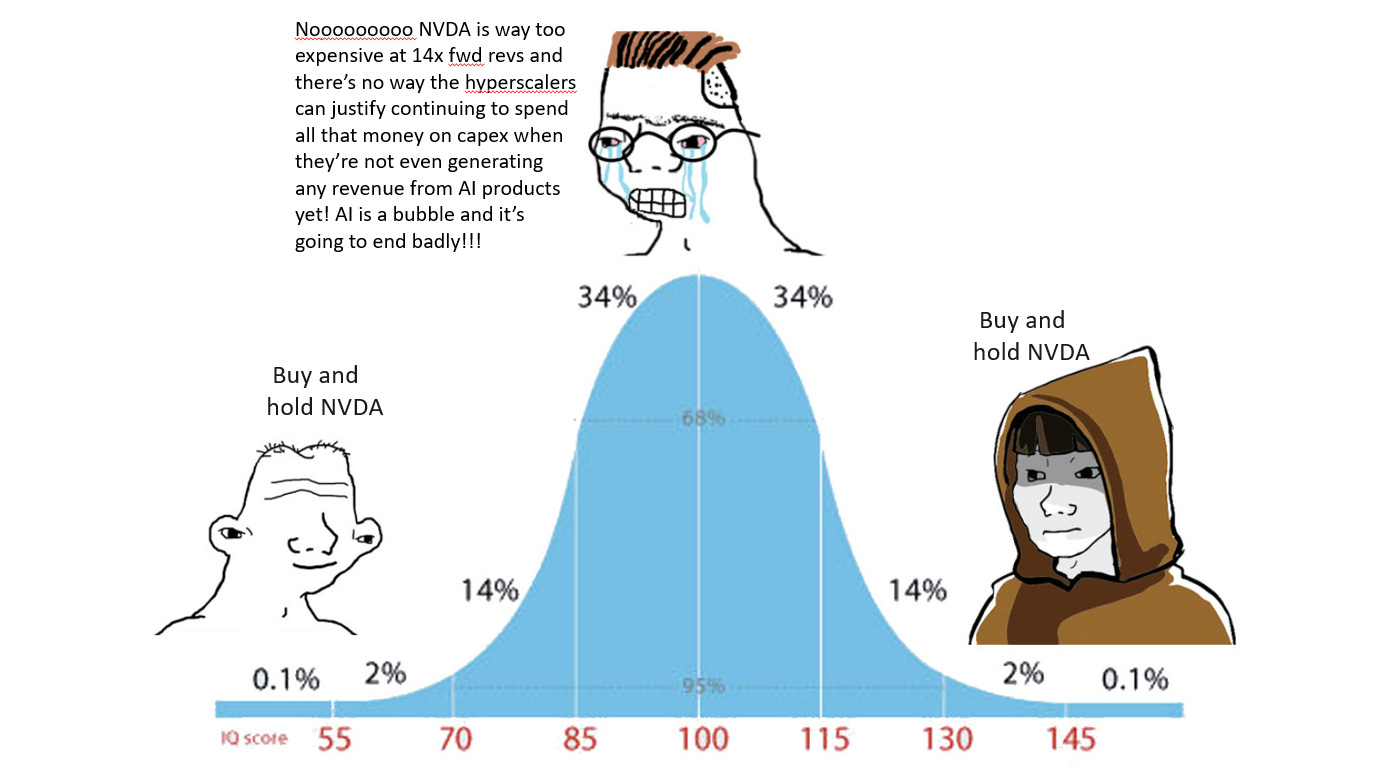

Many will argue we’re already in an AI bubble. They will point to NVDA currently trading at “just” 14x forward revenues, seemingly grossly overpriced AI-adjacent stocks such as SYM 0.00%↑ and AI 0.00%↑ , and the NASDAQ index approaching it’s November 2021 all-time highs even as interest rates have increased to 5% and many predict on oncoming recession.

But, as Doug Clinton of Deepwater Asset Management notes:

In 2000, the Nasdaq peaked at a P/E of 200. It trades in the 30s today, so the Nasdaq would have to increase almost 6x from here to trade at the Dotcom peak. NVDA trades at roughly 35x forward earnings. In 2000, CSCO traded at around 100x forward earnings. So, NVDA would have to increase another 200% from here to get to CSCO-level craziness.

AI might be frothing, but objective comparison to a bonafide bubble says we’re nowhere near roaring insanity. The current AI bubble is closer to 1995 than 2000 using the Dotcom boom as a comparison.

The macro setup for the AI bubble is eerily similar to the backdrop of the early 90s too, which creates the hardest part of timing when to get aggressively long AI.

In 1994, the US economy was a few years into recovery from the 1991 recession, but inflation was elevated at 3%, and the economy was hot. The Federal Reserve started raising interest rates in ‘94, taking rates up ~3% in about a year. The result was a “soft landing” for the economy that slowed growth and avoided recession. Sounds a lot like 2023 as economists debate the possibility of a soft landing in the face of rapid interest rate increases over the past year plus.

The similarities in economic backdrop between the 1990s and 2020s highlight two important things relative to the coming AI bubble.

First, zero rates help form widespread asset bubbles like the Everything Bubble of 2020-21, but they are not a necessary condition for a technologically driven asset bubble. Between 1995-2000, the lowest 10-year yield was around 4.4%, not far from where we are now. The 10-year spent much of the early-to-mid part of the Dotcom bubble above 5.5% and even spent some time around 7%.

Rates might feel oppressive now vs the zero we’re used to, but mid-single digit rates won’t stop an AI bubble.

Second, a soft landing in ‘94 provided fertile economic ground for the formation of the Dotcom bubble. Counterfactually, it’s hard to say whether or not the Internet boom would have happened the same way if the US economy went into recession in the mid-90s. Perhaps the Internet bubble would have been delayed or temporarily crushed. It would not have been avoided.

I want to expand on those last two points.

Many see the current high-interest rate regime we’re in as being restrictive. And they might be right! We’re certainly not in a TINA (there is no alternative) investment landscape any more when it comes to the stock market.

But I’d argue it’s the rate of change of interest rates that matters more for investor behavior and psychology, than the absolute level of interest rates.

Humans are exceptionally adaptable. Investors will adapt to the new rate environment rapidly, if they haven’t already. Many individuals and large pools of capital alike have likely already shifted from stocks into money market funds and bonds yielding 5%.

What do you think they’re going to do when AI stocks start taking off in their face again and they’re caught underweight (like I was in 2023, mind you)?

They’re going to trade their 5% bond yield for tech stocks, because guess what — tech stocks still offer better than a 5% rate of return.

Who is to say what happens over the next year? It is very possible that we have a Fed/macro-induced stock market drawdown which will provide a better entry point for the coming AI bubble.

I’m not saying that if you go all-in now, there’s not potentially going to be pain.

But, it is also very possible that OpenAI releases GPT-5 before the end of the year and it’s capabilities are such that it’s all anyone can talk about around the fireplace at Christmas.

GPT-4 is already enabling individuals to train personal AIs to behave like they do, acting as digital decision-making duplicates.

This new technology is evolving faster than anything I’ve ever seen, and between megacap tech capex and venture capital, the capital pouring into it is more than anything I’ve ever seen.

As such, I think it is prudent for investors with an appropriate risk tolerance and time horizon to error on the side of being early, than risk being late.

That said, I believe we are early, there will be many breakouts and shakeouts, and opportunity will abound.

Again, per Clinton:

Bubbles last longer than rational minds can fathom.

AI won’t be different. It will boom into a bubble just like the Internet because that’s what must happen for the technology to reach its potential. AI valuations will get beyond silly, and they will come back to earth. The alpha-seeking bubble rider must sense the peaks of insanity, which can only be felt through intuition, not logic.

The biggest stock market bubble of our lifetime is staring you in the face.

Don’t overthink it.

Loved this and generally makes sense. One thing:

“Humans are exceptionally adaptable. Investors will adapt to the new rate environment rapidly, if they haven’t already. Many individuals and large pools of capital alike have likely already shifted from stocks into money market funds and bonds yielding 5%.”

Is this empirically true? We entered ZIRP policy in 2009 but it took several years (during which first derivative on rates was zero) for investors to appreciate what that should mean for equity multiples.

As for investors rotating into bonds, most of the charts I see still show equity allocations as percent of overall portfolio near/at all-time highs. (Obviously that’s tough because m2m impacts if, so maybe inflows/outflows are better metric, but haven’t seen/heard about huge equity fund outflows and bond fund inflows.)