Sunday Dump

Stocks Fall, Bonds Plummet, Gold and Bitcoin Rally, Upcoming Catalysts

Three weeks ago I outlined a number of crosscurrents to market liquidity currently pulling in different directions and gave a summary of how I was defensively postured with a 25% cash position and no net equity exposure.

To recap, at the time (Oct 1) I was hedging out my long equity exposure entirely with QQQ puts in light of upcoming negative catalysts to liquidity, including California taxes due on October 16, the restarting of student loan payments and continuing bond issuance from the Treasury.

I concluded with the following view:

My base case is still at some point (soon-ish) we get a spike in bond yields and a sharp drawdown in stocks, forcing the Fed to step back in with QE and away we go.

The Fed tells the market when it’s going to do QT.

The market tells the Fed when it’s going to do QE.

Thus the large 25% cash position — 5.5% return in money markets isn’t the worst place to hide while sitting and watching how things play out.

A weak 30-year bond auction on October 12 sent yields higher across the curve and stoked fears for the potential of a ‘failed auction’ for treasuries, like the UK saw for gilts a little over a year ago, forcing the Bank of England to intervene with emergency QE in the middle of their fight against inflation.

I think this was evidence that we are ever closer to the bond market similarly crying uncle in the US, and forcing the Fed back into QE.

Market Update

Since my last post on October 1, the QQQs have fallen only 1%, despite surging bond yields and a war breaking out in the middle east. It feels worse though. After a relief rally to begin the month, the QQQs have fallen 4% in the past four days.

We ended this past week with the 10-year pushing to new highs, touching 5%:

And the massive rout in the long bond continuing with the TLT 0.00%↑ ETF now in a >50% drawdown (yield-adjusted) from its March 2020 high:

It’s not as bad for bond holders as bitcoin hodlers this cycle quite yet, but we’re getting close with bitcoin currently sitting 56% below it’s all-time high.

I repeat: US treasury bonds have performed nearly as poorly as bitcoin this cycle.

Imagine telling someone that a year ago.

I think within another week or two this will flip, bitcoin will be outperforming bonds from peak-to-market, and you’re going to see a lot of mention of that on X with the potential for a bullish bitcoin narrative to take root.

Bitcoin’s cousing gold has also ripped off the lows this month, performing like you would expect it to as a geopolitical hedge as conflict has broken out in the middle east, but also potentially smelling out and front-running coming Fed liquidity?

Bitcoin has followed suit, decoupling from the stock market and outperforming other cryptos, although there are more crosscurrents in play for bitcoin than gold at the moment, including increasing odds of the SEC approving a spot bitcoin ETF in Q1 2024. A fake news report that they had already done so sent BTC rallying above $30k this week before giving back some of the gains once the report was proven to be a hoax. However, as I write this on Saturday afternoon 10/21 bitcoin has rallied back above $30k and is looking to take out the yearly high around $32k.

I think bitcoin and gold are peaking around the corner, and smelling out the coming end game in the bond market of more QE.

Positioning

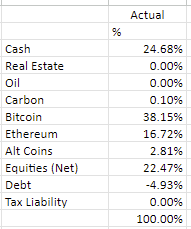

If you recall, I relayed three weeks ago (10/1/2023) I was expressing my near-term bearish view on bonds and equities through a tactical overweight to cash and by hedging out all of my equity exposure with QQQ puts expiring October 20:

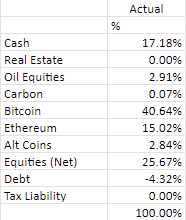

My updated positioning is as follows (10/21/2023):

I see a number of catalysts for bond yields to continue higher and force more stock market weakness in the month ahead, and as such I have rolled my QQQ puts and continue fully hedge my stock portfolio via $350 strike QQQ puts expiring Nov 3 and Nov 17. These puts have a delta of -0.35; my negative equity exposure will increase as the market falls and decrease as the market gains.

(As a quick aside, this is one reason I prefer being long puts to shorting for near-term hedging: with options, your position size naturally increases the more right you are and naturally decreases the more wrong you are. Contrast this to a short position, where the opposite is true: the more right you are, the smaller your position gets; the more wrong you are, the larger your position gets. For near-term hedges I want to lean into the near-term trend.)

I’ve allocated some cash to XLE 0.00%↑ to express a view on a higher oil price as war breaks out in the middle east. I’m also wary of the risk that Russia weaponizes energy this winter, potentially decreasing oil and gas exports (except for to China) to force higher energy prices as cold weather sets in across Europe.

Bitcoin, my largest position, has outperformed, up 12% month-to-date, and as such has grown as an overall % of my portfolio.

Upcoming Catalysts

Here is what I have my eye on in the coming month:

This week: potential for post options expiry volatility. A lot of options expired on Friday 10/20, which can signficantly shift market-wide positioning and create conditions for heightened volatility. I think there’s an increased risk of fireworks this upcoming week.

November 1: FOMC interest rate decision. Jerome Powell said in a speech this week effectively that they are done raising rates for the time being, but that they don’t view current rates as too high. As such, I don’t expect a rate hike, but markets will likely trade on commentary on the future path.

h/t @Barchart November 1: Quarterly Treasury Refunding Announcement. I think this is more important than the FOMC. If the Treasury announces it intends to issue more securities than the market is anticipating, this could accelerate the sell-off in the bond market. I think there is signficant risk of this happening because of the looming government shutdown on November 17. The Treasury cannot risk running out of money during a prolonged shutdown, and as such may seek to increase issuance in early November to levels that the market has trouble absorbing.

November 17: US federal budget deadline. Without a House Speaker, increasing odds that the government shuts down on November 17.

November 17: another monthly options expiry, always a time for caution.

Israel/Palestine: potential for the conflict to spread. Risk to oil prices spiking, which would be inflationary and potentially further pressure bond yields.

Gold/bitcoin: if these assets continue to rally, it would lead me to strongly consider allocating to TIPS via the TIP ETF, as my interpretation would be these assets are signalling a nearing top in real yields.

Summary

In sum, my ultimate view of a bond-yield induced market panic being met with a return to QE and sky-rocketing asset prices off the bottom remains unchanged.

Everything I’m seeing currently supports that view:

Treasury auctions are showing signs of weakness

Interest rates are shooting up to new highs

High-yield credit spreads are widening, confirming equity market weakness

Gold and bitcoin are rallying

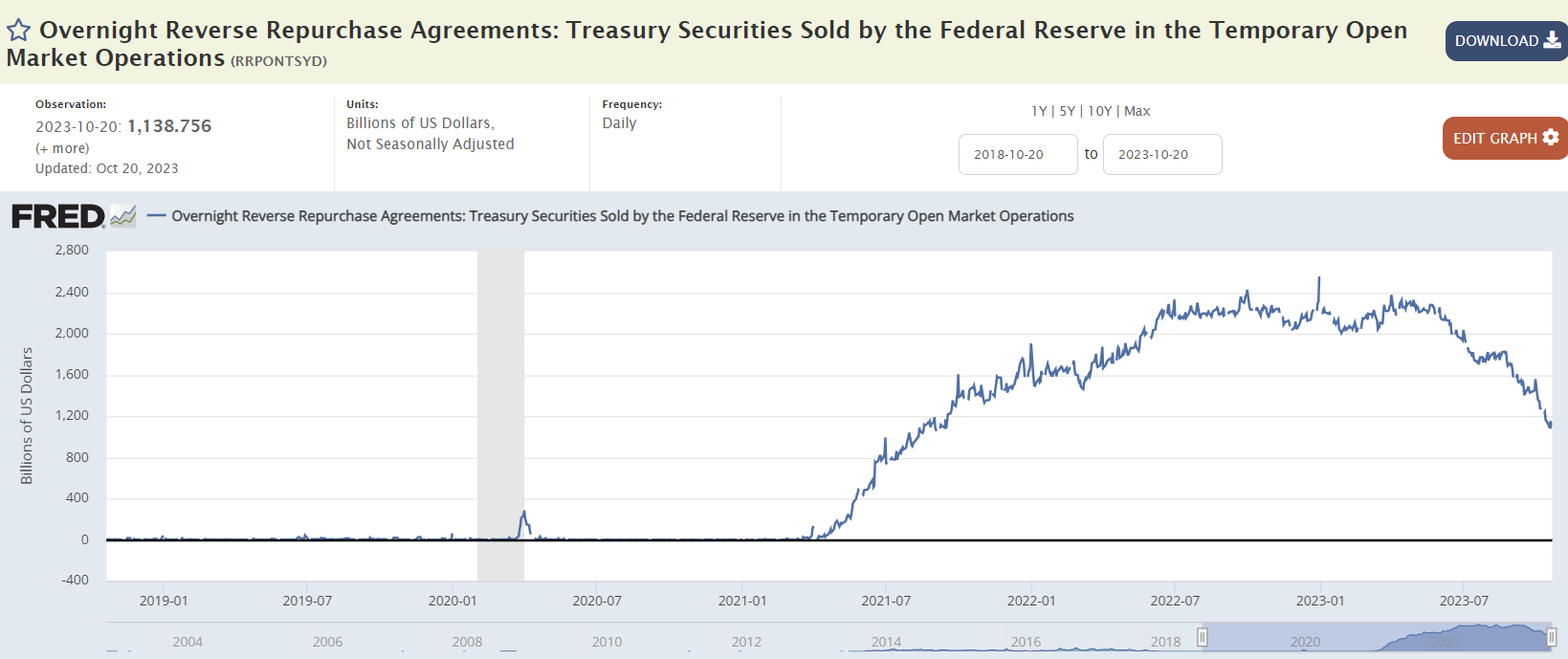

The RRP continues to draw down, rapidly removing the last remaining source of liquidity for markets. In fact, I’m increasingly of the view that when the RRP is depleted might be when markets really go into a tailspin. If this the case, we might have another 3-6 months of chop/treading water/slow bleed before real pain sets in.

As such, I remain record-cautious (for me) in the short-term, with high cash and equity market put option exposure, while I wait for my thesis to play out. If and when we do get an acute equity market sell-off combined with a pivot to QE, I remain ready to switch to max long.

Until that happens, I think patience and caution are warranted.