Part 2: Replacing Stock with Options + Cash

And How to Leverage your Brokerage Account for a Free Loan

In All of the Reward and None of the Risk* last week I mentioned how I looked into replacing my ARKG exposure with call options, but the options were too expensive as the implied volatility was too high.

So what if we instead got paid the option premium instead of being the payer, capturing the value of the high implied volatility without taking on the risk of said volatility any more so than we were by holding stock in the underlying.

Introducing: synthetic longs and free leverage on your margin account.

Options for Civilians

A “synthetic long” is an options position which creates the same payoff as simply being long the stock. It is entered into by being long a call option and short a put option on the same underlying with the same strike and expiration date.

The benefits of utilizing options to create the long stock exposure are the same as we covered last week - due to the embedded leverage in options, you can get the same price exposure as owning some notional amount of the underlying stock by only putting up a fraction of the capital. If you have a good vehicle to invest the leftover capital in this can be a good strategy that generates excess returns over simply holding stock.

For example, let’s look at the ARKG 01/19/2024 $30 strike options. As I write this on the morning of June 7, ARKG is trading at $32.44. The premium on the $30 strike call option is $9.55 and the premium on the $30 strike put option is $7.70. The call premium being > the put premium means opening up a synthetic long position of 100 shares of ARKG using these options would be net debit to our account of $185, i.e. it would cost us $185 to get $3,244 of ARKG exposure through options and we would have 100 x $32.44 - $185 = $3,059 leftover. We pay net $185 because we pay 100 * $9.55 = $955 for the call option and we get paid 100 * $7.70 = $770 to sell the put option.

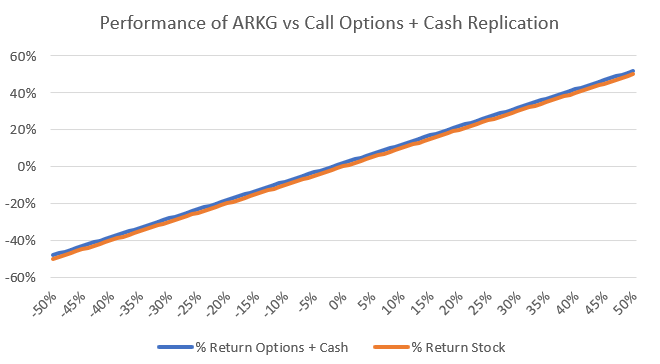

The payoff curve looks like this:

Again, the y-axis is the % price performance of the portfolio and the x-axis is the % price performance of the underlying stock. The orange line represents a portfolio of the underlying stock, so y = x for the orange line.

As you can see the payoff is the same. As ARKG declines, we can only lose a maximum of the premium paid of $955 on the call option. On the short put position, our max loss if the ARKG were to go to zero is 100 x strike minus premium collected. In this case 100 x $30 - $770 = $2,230. So our max loss on the whole trade is $3,185 — $3,000 plus the net debit we paid to put on the trade of $185. Notice how $3,000 is also what we would lose if we were long 100 shares of ARKG from $30 and the price went to $0. Hence, synthetic long.

On the upside, the max we can make on the short put is the premium we were paid for it, or $770. Remember a put gives our counterparty the right but not the obligation to sell or “put” us 100 shares of the underlying ARKG at the strike price. If the market price > the strike price, our counterparty would simply choose to sell their shares in the market, since they could get a better price that the $30 they could get from exercising their option. The max we can make on the call option is theoretically unlimited, just like owning the underlying stock is.

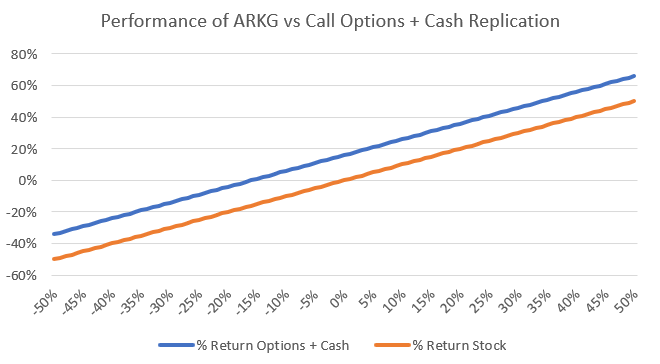

The above payoff curve assumes no return on the cash saved by using options. But remember, the whole point of doing this is we can get 9% return on cash by holding USDC on Voyager (plus $50 BTC if you create an account using this link or code 2E702D at sign-up) . If you didn’t read Part 1 to this post, the reward tiers for holding USDC on Voyager currently are:

When we plug this return on cash into the payoff model, we get this:

Now our blue line options + cash return is noticeably better than our stock return for any outcome (assuming we get the rates in the above tiers for the duration of our trade, which in this case is modeled to be 1.6 years to January 2024). It’s actually 16% better for all outcomes — quite a trade if I do say so myself.

But we can do even better.

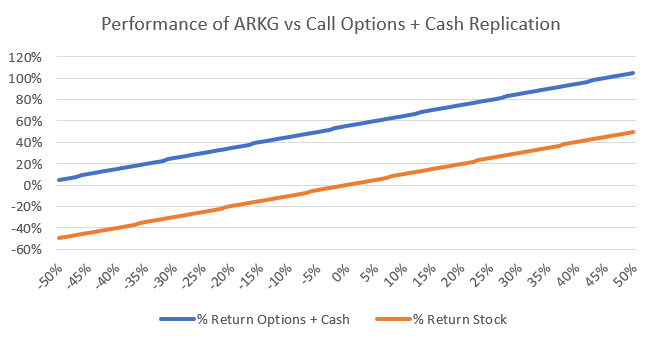

One thing about synthetic long options spreads is they work for any strike and expiry, so long as the strike and expiry on the long call matches the short put. So, you can imagine going down to the highest strikes in the chain where the calls cost a little and the puts cost a lot and earning a large net credit to put on this trade, as opposed to paying the small net debit as we did in the example above.

The Trade

Not financial advice!!! You must know what you’re doing with options, margin and leverage to engage in this trade.

Imagine in your you’re long 100 shares of ARKG @ $32.44 in your margin account for a notional position of $3,244 and you want to replace your exposure with a synthetic long options spread.

SELL: 100 shares ARKG @ $32.44 for $3,244

BUY: 1 01/19/2024 $119.62 strike ARKG call option @ $0.55 for $55

SELL: 1 01/19/2024 $119.62 strike ARKG put option @ $87.65 for $8,765

BUY: $11,954 USDC on Voyager

$119.62 is the highest strike option available on ARKG for the 01/19/2024 expiry, and thus generates the largest net credit for the participant entering a synthetic long options spread.

In selling our ARKG position and a far in-the-money put option for a combined $12,009 and paying a mere $55 for the far out-of-the-money call option, we generate $11,954 in cash on a $3,244 position. Daddy like.

Now, we cannot necessarily just take that $11,954 out of our account, as the short put option creates a large short position which we need sufficient margin to cover. As such, this trade works well if you’re replacing a smaller position in a larger portfolio.

For example, let’s say ARKG was a ~3% position in a $100k stock portfolio in a margin brokerage account. Before this trade, you have $100k in long stock positions including a $3,244 position in ARKG. After this trade, you now have $100,000 - $3,244 = $96,756 in long stock positions, a long call option worth $55, a short put option worth -$8,765, and $11,954 in cash. $96,765 + $55 - $8,765 + $11,954 = $100k.

If you have a margin account, you will be free to withdraw the $11,954 in cash and go invest it in USDC. Your account value will be reduced by $11,954 and now be $88,046 but you will still have $100k in notional long stock exposure because of the leverage embedded in your synthetic long on ARKG.

You will now have a margin maintenance requirement that needs to be monitored. You are at risk of a margin call.

Check with your broker’s margin requirements. In this case, you’re leveraging your account by ~12% so you should be comfortably within requirements and only at risk of a margin call if your portfolio drops by a significant percentage (50%+). But I cannot stress this enough this is only for experienced traders who know what they’re doing with options and margin leverage!

Necessary caveats out of the way, here’s the magic trick…

On one hand, this is not much different than just taking out a margin loan on your account for $12k. Thing about a margin loan though is you have to pay interest on it, significantly eating into or completely wiping out the 9% return you can get on USDC depending on what interest rates your broker charges on margin loans. My broker Fidelity, for example, charges a base rate of 7.825%.

By entering this trade and creating a net credit of ~$12k, we are able to maintain our net long exposure to ARKG while generating $12k of cash in the account. And we can withdraw this $12k without paying any interest on it! We’ve effectively used options to generate a free loan against our stock portfolio which we can now earn a 9% spread on, without sacrificing any equity exposure.

In this case, our $11,954 USDC earns $1,790 over our holding period of 1.6 years (til Jan 2024). $1,790 against our original $3,244 ARKG position is 55%.

We can increase our returns on a $3,244 position in ARKG by $1,790 or 55% by entering into this trade instead.

Disclosure: the author is long Voyager’s VGX token, USDC, ARKG+calls and short ARKG puts.

Disclaimer: nothing published in this newsletter is investment or financial advice. The author may be long or short any of the securities or assets discussed at any time before or after publishing.