Bitcoin Announces Q2 2022 Results

Bitcoin Announces Q2 2022 Results

GLOBAL, Jul. 12, 2022 — Bitcoin (CRYPTO: $BTC) today announced financial results for the second quarter ended June 30, 2022.

Second Quarter 2022 Financial Results:

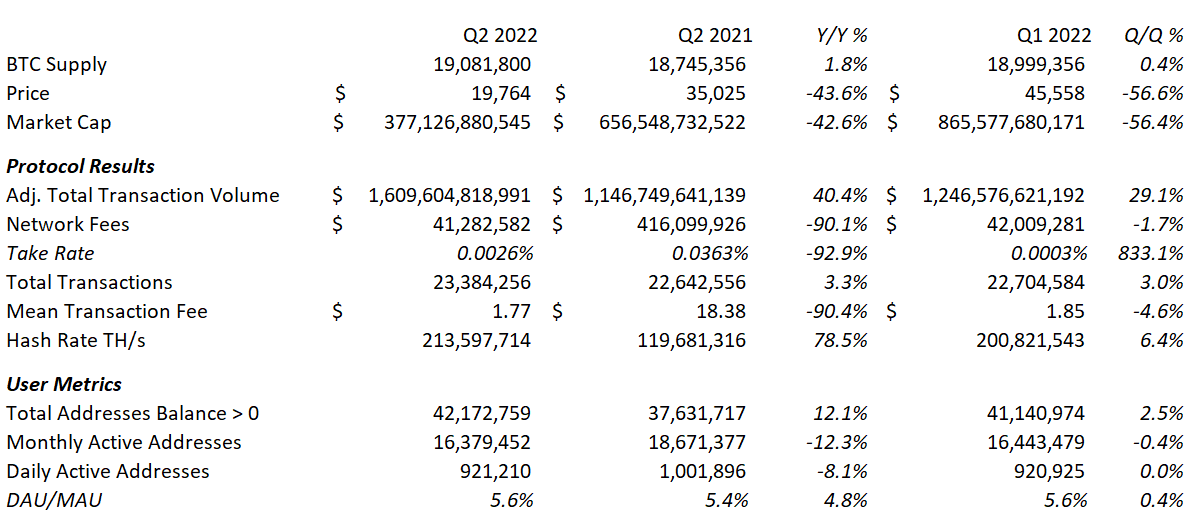

Revenue: network fees in Q2 were $41 million, down 90% year over year from $416 million in Q2 2021.

Share Count: BTC supply at the end of Q2 totaled 19.1 million, up 1.8% year over year from 18.7 million in Q2 2021. The supply of BTC is capped at 21 million.

Total Transaction Volume: value settled on Bitcoin in Q2 was $14.4 trillion, up 91% year over year from $7.5 trillion in Q2 2021.

Adjusted Transaction Volume: change- and entity-adjusted transaction volume, an estimate of true economic value transfer comparable to total payment volume on other payment networks such as Visa and Mastercard, in Q2 was $1.6 trillion, up 40% year over year from $1.1 trillion in Q2 2021.

Transactions: the number of transactions in Q2 was 23.4 million, up 3.3% year over year from 22.6 million in Q2 2021.

Transaction Fees: the mean transaction fee in Q2 was $1.77, down 90% year over year from $18.38 in Q2 2021.

User Metrics:

Average daily active addresses in Q2 were 0.92 million, down 8% year over year from 1.00 million in Q2 2021.

Average monthly active addresses in Q2 were 16.38 million, down 12% year over year from 18.67 million in Q2 2021.

Total addresses with balance > 0 ended Q2 at 42.17 million, up 12% year over year from 37.63 million in Q2 2021.

Hash Rate: computing power securing the Bitcoin blockchain via Proof-of-Work at the end of Q2 was 214 million TH/s, up 79% year over year from 120 million TH/s at the end of Q2 2021. Blockchain security increases with increased hash rate.

Q2 2022 Highlights and Market Commentary

With the Fed hiking interest rates aggressively to try and tame inflation, Q2 was a tough month for long-duration risk assets and Bitcoin was no exception, with the price falling from $35,025 to a low of $17,592 on June 18th as the Three Arrows Capital (3AC) forced liquidation plunged prices across the crypto space. By quarter end the price had recovered to $19,764, just above it’s 2017 cycle peak of $19,700.

Despite the brutal price action, key network health indicators are still flashing green.

Adjusted transfer volume, a measure of total economic activity being settled on the bitcoin blockchain, grew to $1.6 trillion in the quarter, just shy of it’s quarterly all-time high set in Q4 2021 and an increase of 40% YoY and 29% MoM.

Hash rate, a measure of blockchain security, rose to an all-time high of 214 million TH/s, and increase of 79% YoY and 6% MoM. Miner activity continues and the bitcoin network is as secure as ever, despite the 72% drop in market value.

Total addresses with balance > 0, a measure of network adoption, continued its steady growth to an all-time high of 42 million, up 12% YoY and 3% MoM. Every day new users are stacking their first sats.

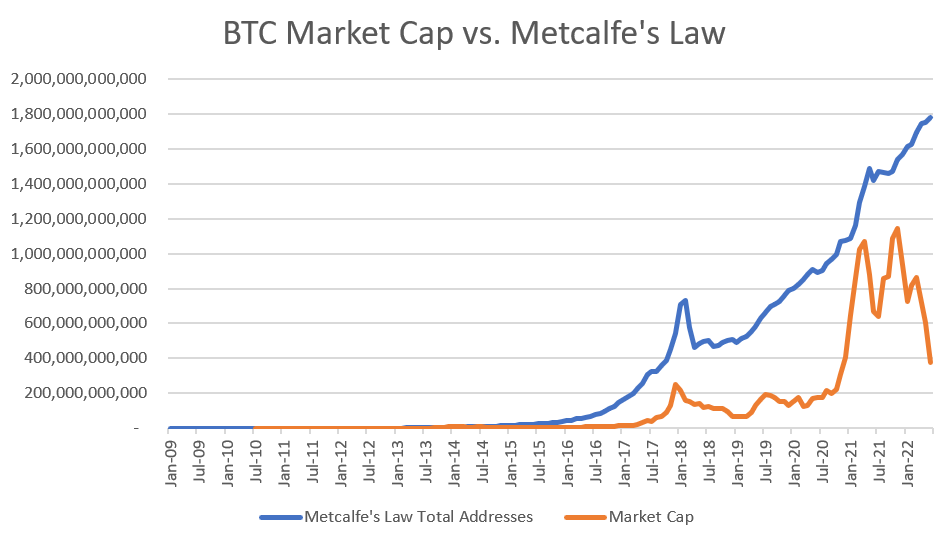

Historically, network adoption has been a leading indicator of positive price movement. In the chart below we can see that bitcoin’s market cap of $377 billion is at its widest gap in absolute terms to the Metcalfe’s Law model in history.

Signs of a Bottom

Though the macro picture always clouds things, there are two on-chain metrics that I watch to signal a cyclical bottom in the bitcoin price.

The first is the Market Value to Realized Value Ratio, or MVRV Ratio.

The MVRV Ratio compares the current market value of a cryptocurrency to the total amount of money invested into a cryptocurrency. When it falls below 1, that means that in aggregate holders are underwater and historically has been a sign of a market bottom. When it’s above 4, that means that in aggregate holders are sitting on >4x profits and historically has been a sign of a market top.

The MVRV crossed below 1 on June 13th and reached a low of 0.84 on June 18th (it probably actually reached a nadir even below that when the price plunged below $18,000, but we only have daily data available for this metric). Previous major market bottoms in 2018 and 2020 saw the MVRV reach 0.7 and 0.9, respectively.

As you can see in the chart below, every time the MVRV has reached below 1 (the dotted horizontal line) has been a significant long-term buying opportunity.

source: Glassnode

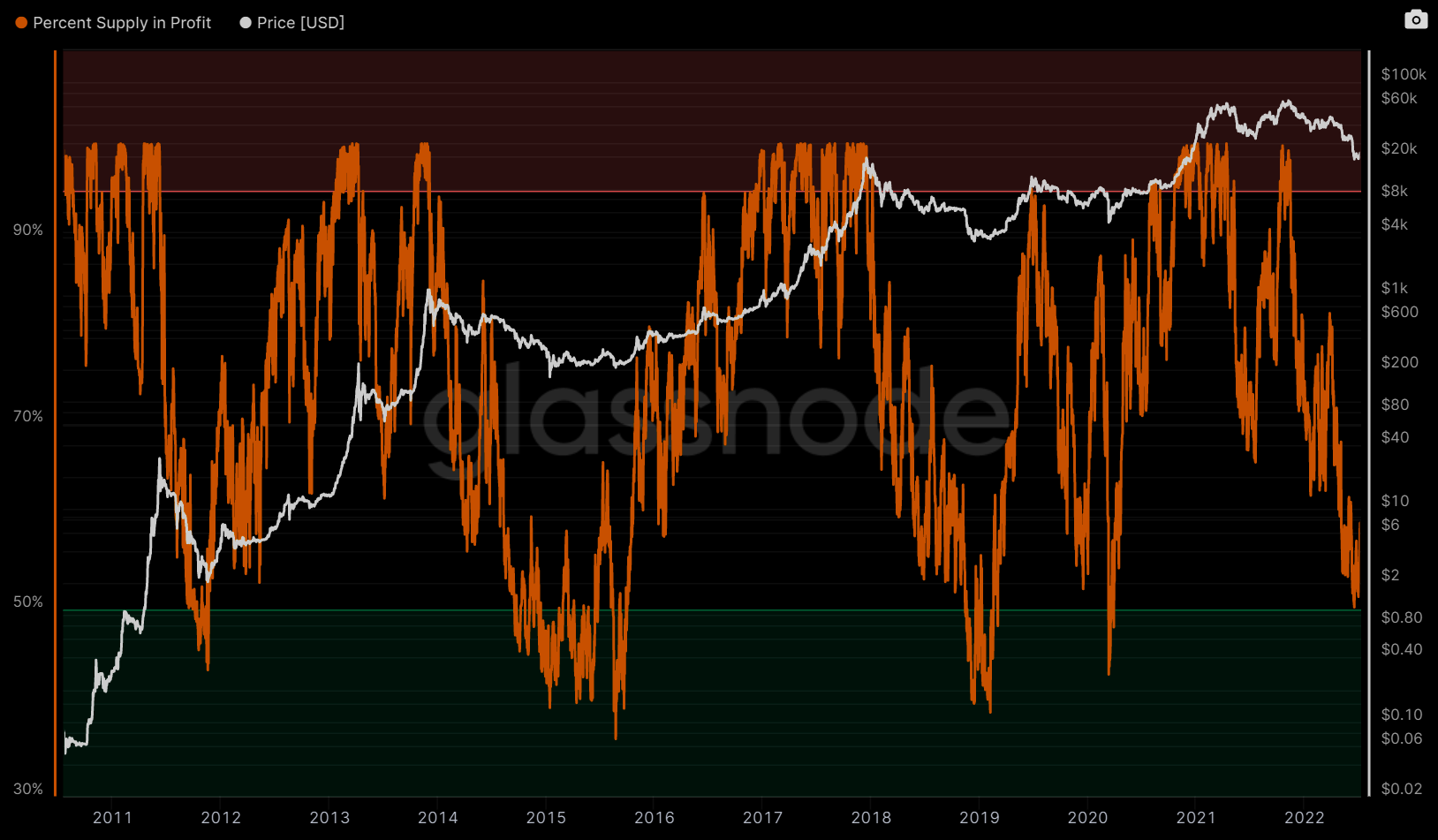

The second metric I watch closely is the Percent Supply in Profit.

Similar to MVRV, this measures how much of the supply is currently in profit, meaning the rest is currently underwater. Whereas MVRV is a measure of how much coins are below cost basis, or the depth of drawdown across holders in aggregate, Percent Supply in Profit is a measure of how many coins are below cost basis, or the breadth of the drawdown across holders in aggregate.

Historically, when this percentage has dropped below 50%, meaning more of the supply is underwater than not, that has been a sign of a market bottom and a great time to buy. Above 95% signals a market top and a good time to sell.

Percent Supply in Profit hit a low of 50% on June 18th, and currently sits at 56%. It has not yet reached quite as low as in 2018 (39%) or 2020 (46%).

source: Glassnode

Finally, Bitcoin aggregate volume across venues reached an all-time high during the 3AC unwind on June 17th. As Alex Kruger @krugermacro on Twitter elaborates on in this thread, the 2nd and 3rd all-time highs in volume came during major market bottoms in March 2020 (pandemic panic) and May 2021 (China bans mining).

Across history and across asset classes, major market bottoms tend to form on record high volumes which signal capitulation.

source: @krugermacro, Twitter, TradingView

Continued steady pace of adoption, on-chain metrics like MVRV and Percent Supply in Profit, record-high capitulatory volumes and numerous bankruptcies and related position unwinds suggest the bottom is in or near for Bitcoin.

SEC Rejects Grayscale’s Spot Bitcoin ETF Application

Putting a nice cherry on top of an anything-but-sweet quarter for Bitcoin, on June 30th the SEC officially rejected Grayscale’s latest bid to turn the markets largest spot bitcoin fund GBTC into an ETF.

Under its current structure, GBTC effectively operates as a closed-end fund with no redemption mechanism. Investors can create new shares of GBTC by pledging spot bitcoin to Grayscale, but investors holding GBTC cannot convert their shares of GBTC into spot bitcoin.

This has caused GBTC to trade recently with a >30% discount to NAV. Converting GBTC to an ETF would allow an arbitrage mechanism to occur between the fund shares and the fund assets and unlock some $4.2 billion of investor value at current prices.

The SEC’s grounds for rejection were that the application did not do enough to prevent market manipulation. I’m not entirely sure what this even means in this context, as Bitcoin is a large and liquid market no more subject to market manipulation than any number of other markets that support ETFs. Indeed, spot bitcoin ETFs have been approved and existed in Europe and Canada for over a year at this point, without problem needless to say.

Brett Harrison, president of FTX, has a good thread calling out the SEC’s hypocrisy on this matter.

Speculation is that SEC Chair Gary Gensler is holding the spot bitcoin ETF approval hostage in return for the SEC garnering greater oversight over crypto exchanges. Whatever the true motivation is, the U.S. is significantly behind the curve on this one and, contrary to the SEC’s purported raison d'etre, domestic retail investors are being substantially harmed by the decision both directly and indirectly.

In addition to the current fund structure trapping $4.2 billion of investor wealth for no good reason (direct harm), it was in part due to GBTC trading to such a significant discount to NAV that 3AC went bust and contagion spread. Before March 2021, GBTC had traded at a significant premium to NAV, and 3AC was known to be heavy in the trade of creating shares at NAV and cashing them out at a premium. When the premium flipped to a discount, this trade turned sour and 3AC incurred significant losses.

Now, obviously, no excuses for the poor risk management at 3AC which led to out and out fraud in an attempt to cover their losses. We’ll never know what would have happened had GBTC been an ETF and 3AC been able to get their value out, but I think it’s fair to say the SEC’s repeated denial of Grayscale over a multi-year period of significant growth in both Bitcoin and GBTC has created an inefficient market structure that has resulted in significant mark-to-market losses for investors, exorbitant realized fees on the only listed spot bitcoin product on the market (2% on NAV = 2.9% on market value at a 30% discount), and contagion across the crypto space.

Grayscale immediately filed a lawsuit against the SEC, with CEO Michael Sonnenstein saying "The SEC is acting arbitrary and capricious by continuing to approve bitcoin futures-based ETFs while continuing to deny spot bitcoin ETFs," in an interview with CNBC. A ruling is expected within a year.

It is remarkable to think about how the SEC has kind of done the opposite of what one might think you would want to do to protect retail investors in crypto. If I were Gary, I think I’d start with allowing GBTC to convert to an ETF and regulating CeFi crypto banks, such as Celsius and Voyager which have frozen customer withdrawals, as banks.

Alas, when blow-ups occur regulation is sure to follow as public sentiment for regulation turns favorable. In the wake of this quarter’s mess I’m sure the regulatory outlook will gain more clarity soon, and I believe thoughtful, sensible regulation will allow (more) institutional money to come into the space and be a tailwind during the subsequent period.

Results Table:

Disclosure: I own BTC

About Bitcoin

From bitcoin.org:

Bitcoin is an innovative payment network and a new kind of money. Bitcoin uses peer-to-peer technology to operate with no central authority or banks; managing transactions and the issuing of bitcoins is carried out collectively by the network. Bitcoin is open-source; its design is public, nobody owns or controls Bitcoin and everyone can take part. Through many of its unique properties, Bitcoin allows exciting uses that could not be covered by any previous payment system.

About this Release

This release is not an official release of Bitcoin or the Bitcoin developer community. The purpose of this release is to provide data and a framework for analysts and investors to think about valuing Bitcoin as they would a publicly traded company, using traditional metrics, multiples and methods. All Bitcoin blockchain data contained in this release was sourced from Glassnode Studio and Messari.

For inquiries please contact the author on Twitter @realzackm.

Disclaimer: nothing published in this newsletter is financial advice. The author may be long or short any of the securities or assets discussed at any time before or after publishing.