With Great Leverage Comes Great Volatility

Will We Get a J or a Hockey Stick?

I recently watched a Real Vision interview with Luke Gromen titled Navigating the Most Dangerous Investing Environment in Decades. It’s behind a paywall, but you can sign up for a free trial to watch the video and I encourage everyone to do so.

I mentioned last week that I do think we’ve reached a momentous occasion for markets and I expect markets from here to quickly (0-12 months) resolve into a J or a hockey stick, i.e. I think we’re going to get a market crash followed by a rip reminiscient of 2020, or possibly we just skip the crash this time because everyone knows the rip is coming on the other side of it.

Luke articulated why he also thinks this is the case with more data, clarity and reasoning than I could ever hope to myself, so below I’m going to paraphrase his argument for my own understanding and, hopefully, my readers’ benefit as well because I think Luke has it 100% nailed.

Powell Could Never Be Volcker

Paul Volcker was the Fed Chairman from 1979-87 who is celebrated in the history books for breaking the back of the inflation of the 1970s and cleaning up the mess left by his predeccesor Arthur Burns. Burns was the Fed Chairman from 1970-78 who is remembered as a abject failure who allowed the inflation of the 70s to get out of hand.

The trope today is that current Fed Chairman Jerome Powell wants to be remembered as Volcker and not Burns, but that was always a false choice. Being Volcker is simply not an option for Powell because the parameters of the game have changed, for reasons discussed below. The true choice facing Powell was always Burns or Benjamin Strong, who was the first governor of the Federal Reserve Bank of New York from 1914-1928 and who’s tenure ended in the Great Depression.

As we sit here today, the Fed, in Powell’s efforts to be Volcker, has hiked interest rates to 5% but headline CPI inflation still sits at 6% (probably closer to 4% based on real-time indicators). Meanwhile the U.S. has debt-to-GDP of 125% and is running an annual deficit of 8% of GDP.

This puts Powell between a rock and a hard place: the Strong path or the Burns path.

The Strong Path: Hike Rates Enough to Cause a Recession and Bring Down Inflation

This is the Strong path disguised as the Volcker path, and the path we’re currently on. The reason we can’t do today what Volcker did in the late 70s/early 80s is that the parameters of the game have changed.

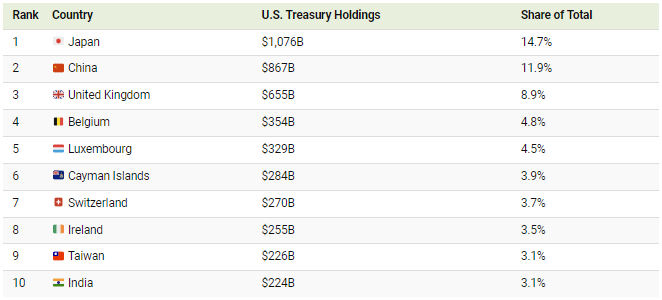

When Volcker took office he was operating with 30% debt to GDP and a 0.3% annual deficit. This meant he could raise rates and cause a recession (i.e. negative GDP growth) to bring down inflation and the government could still finance itself by increasing the deficit, which it did to 2-3% during the recession of the early 1980s, because there were plenty of natural buyers for U.S. treasuries, led by foreign governments running current account surpluses with the U.S., most notably at the time Japan.

The difference today is that Powell is operating with 130% debt to GDP and an 8% deficit at peak tax receipts in 2022 which were the 2nd highest they've been in 70 years as a percent of GDP. During the last three recessions the deficit spiked 6%, 8%, and 12% (notice the trend?). Deficits typically spike during a recession due to a combo of higher fiscal spending (to stimulate the economy) and lower tax receipts. So a recession today probably means the deficit spikes to 14-20% of current U.S. GDP, which is about $24 trillion.

What this means is that in this scenario the U.S. is going to have find financing for $3.4 - $4.8 trillion in new debt issuance in a world where foreign central banks are net reducing by ~$1 trillion/year, the domestic banking sector is selling treasuries to shore up their balance sheets at call it ~$0.5 trillion/year, and the Fed is saying they're still going to be doing QT of ~$1.2 trillion/year. Add it all up and that's ~$6 trillion of new financing net of QT, or $500 billion a month of QE if the Fed were to finance it all themselves. The current Fed balance sheet is $8.7 trillion, so we’re talking about potentially expanding it by 70% to finance one year of fiscal deficit spending in a recession.

Now the private sector can finance some of that, but global private sector GDP is $85 trillion, so it would need to grow 7% to add all of it onto its balance sheet. But guess what, we’re not growing 7% because, remember, we’re in a high rates-induced recession to bring down inflation. And the number one “private sector” buyer of U.S. treasuries, commercial banks, are now unloading to shore up their balance sheets which were rekt by high interest rates!

Okay fine, so the private sector/foreign investment funds will just need to sell stocks to fund treasuries. Simple enough right?

Well, accordingly to Luke, 200% of the annual growth in PCE (personal consumption expenditure) in the U.S. is accounted for by net capital gains and taxable IRA distributions. This means that growth in domestic consumer spending is completely funded by gains in asset prices. So if asset prices fall, consumption is going to fall. If consumption falls, GDP falls. If GDP falls, tax receipts fall and now that $6 trillion deficit is a $7 trillion deficit, U.S. needs to issue even more treasuries, private sector needs to sell even more stocks, and you enter a debt death spiral.

Not good, and that’s only half the equation.

The above is solely an accounting of brand new annual debt financing the U.S. would need to get through a recession. Increased debt servicing costs at higher interest rates is another unsustainable problem altogether.

For the past 40 years before 2022, the growing national debt has been offset by lower interest rates so that debt servicing costs as a percent of GDP have been able to remain steady, around 2% plus or minus 1%.

But that’s all about to change.

Even with a still-low average interest rate of 1.64%, interest is already the third largest expense of the U.S. government behind entitlements and military spending as of September 2022, accounting for 7.5% of the budget.

As that debt matures and the U.S. has to refinance at higher rates, interest costs are going to increase and to fund them either:

A) Taxes need to increase. Remember the treasury just took in the most taxes in 70 years as a percent of GDP in 2022, fueled by record capital gains in 2021, and in a recession you’re looking at lower tax receipts.

B) Spending on entitlements or defense needs to be cut. Problem is, entitlements are indexed to cost of living and inflation and entitlement spending has been growing at 10% a year before these adjustments kick in in 2023, and, oh, by the way, we’re financing a proxy war against Russia and have sent Ukraine $100 billion over the past 12 months.

C) The deficit has to increase.

$9.5 trillion of the national debt either matures or re-sets to the prevailing rate in 2023. Refinancing $9.5 trillion of 1.64% debt at 5% will add $320 billion in debt service costs in 2023, bringing debt service costs from 7.5% of total spending to ~12.5% of total spending. Run this dynamic foward three years and the interest on the national debt runs about $1 trillion dollars annually, roughly equal to current spending on defense and higher than current spending on Medicare.

Finally, this is just the U.S.! Extrapolate all of the above for the rest of the western world and the global deficit financing needs only grow.

What this means is Powell can't keep interest rates highorrr for longorrr because the result would be unsustainably high debt servicing costs which would necessitate a painful cut to spending (22% of GDP), a drastic increase in tax revenue, or both. Either way, we’re looking at a recression, and probably a big one.

But we can’t have a recession because falling GDP would add to already high annual deficits and there is simply not enough global balance sheet to take on $6-$7 trillion annually in new U.S. treasury issuance (absent central bank balance sheet expansion of course, we’ll get to that next).

So, Powell can’t be Volcker.

He can’t raise rates and cause a recession to bring inflation down. If he continues to try, he will cause another depression and be remembered in the same gasp as Ben Strong.

The Burns Path: Print The Money

The other path is more QE and Yield Curve Control (YCC). This is the path we’ve started down with the BTFP - it is a soft, disguised form of YCC.

By allowing the banking system to fork over their U.S. treasuries at par for cash, the Fed has created an environment where the banks don’t need to sell their treasuries to meet liquidity needs. Selling treasury bonds would push prices down and yields up, so the BTFP implicitly puts a cap on bond yields — YCC.

Moreover, the term of the BTFP is ostensibly one year, meaning the banks have to repay the loans and take back their collateral a year hence. But the fundamental problem that necessitated the need for the BTFP in the first place is high interest rates. High interest rates incentivize the public to move their cash out of non-yielding bank accounts and into t-bills or money market funds (MMFs). That incentive isn’t going away unless interest rates on deposits become competitive with rates on MMFs, which can’t happen at least until the yield-curve steepens (currently it’s inverted). This means either short-term rates need to come down or long-term rates need to go up in an environment where the Fed is actively hiking rates on the short end and suppressing rates on the long end.

I’ll say that again. The Fed is currently hiking interest rates and at the same time expanding their balance sheet. They’re trading against themselves.

Something’s gotta give.

Unless the Fed lowers rates — I’d argue to zero to incentive deposits to come out of MMFs and back into the baking system — in a year’s time when the BTFP term is up they’re going to have to extend it or we’re going to find ourselves right back in the same situation as we did a couple weeks ago, with banks needing to firesale their bond portfolio and/or going bust.

This is how temporary, emergency policy becomes permanent policy, and how the BTFP becomes outright QE.

So, it looks to me like either rates need to be cut dramatically or the balance sheet needs to expand. And, for reasons we covered above, the answer is probably both need to occur within the next 12 months and likely much sooner.

When we have an asset inflation driven economy and asset inflation driven tax receipts, assets need to inflate!

The only question is how readily is Powell going to embrace his reality?

Will he persist stubbornly in his fight against inflation, causing a recession and attempting to bankrupt the U.S. in the process, in his quest to be remembered as Paul Volcker?

Or will he accept the realities staring him and the global economy in the face, start printing money and cutting rates with CPI at 6%, and risk being remembered as Arthur Burns?

In the former scenario we get the J. A deflationary crash, then money printer go brrr.

In the latter we get the hockey stick. Straight to money printer go brrr.

When you have a system with extreme leverage, you get extreme outcomes. Extreme to the downside and extreme to the upside.

At the end of the day though, the Big Print is coming and the longer Powell waits, the bigger it will be. We know this because no sovereign nation has ever defaulted on its debt for lack of printing money.

We will know for sure it is time to buy everything under the sun (except bonds!) the second Powell cuts rates to zero and announces QE. Until then, I think extreme caution is warranted on both sides of the coin. You don’t want to be caught levered long in a deflationary crash, and you don’t want to be caught short in the mother of all rips.

The Paths Less Traveled

There are two other potential paths out of the current predicament that bear brief mention.

One is a productivity miracle that allows us to suddenly grow real GDP way above trend — i.e. grow our way out of the debt. I’d say this is highly unlikely and would need to arrive fast, but with headlines about AI and nuclear fusion who knows?

The other is substantially debasing the money in one fell swoop. This is effectively what the U.S. did in 1933 and again in 1971 in going off the gold standard. Credit, again, as in the rest of this post, to Luke Gromen in this interview at the 1:03:00 mark for this because I had no idea.

The mechanism would be as follows: in the accounting manual for the Fed there is a paragraph that states that the Treasury can instruct the Fed to “remonetize” the U.S.’s gold. Just simply write it up to whatever U.S. dollar price they want. The accounting treatment of that is you credit the Treasury General Account with the increase in the price of gold, times the United States’ 261 million ounces of gold.

So, every $4,000 the Treasury instructs the Fed to write up the price of gold to results in ~$1 trillion going into the U.S. Treasury. The Treasury could write up the price of gold by $20,000, receive $5 trillion free of debt, use that to reduce debt-to-GDP either by reducing debt (buyback $5 trillion of U.S. treasuries at the current 70-80 cents on the dollar) or growing GDP (infrastructure spending), and give themselves some wiggle room to normalize monetary policy.

In fact, after learning about this, it sounds like a pretty compelling outcome. I might go out and buy some gold bars.

Gold is currently $2,000/oz.

This outcome would represent debasing the money all at once, instead of over time through money printing. In this world, as in the other world described above, the winners are the owners of scarce assets — bitcoin, gold, real estate, stocks — and the losers are the debt holders.

Source: Visual Capitalist

Hmmmm…